A Comprehensive Self-Help Credit Union Review

The institutions we bank with can make all the difference when it comes to our credit. The whole point of building credit is to get the most favorable rates on financial products. And, some of the best institutions are credit unions — Self-Help Credit Union comes to mind, particularly for those on the credit repair journey.

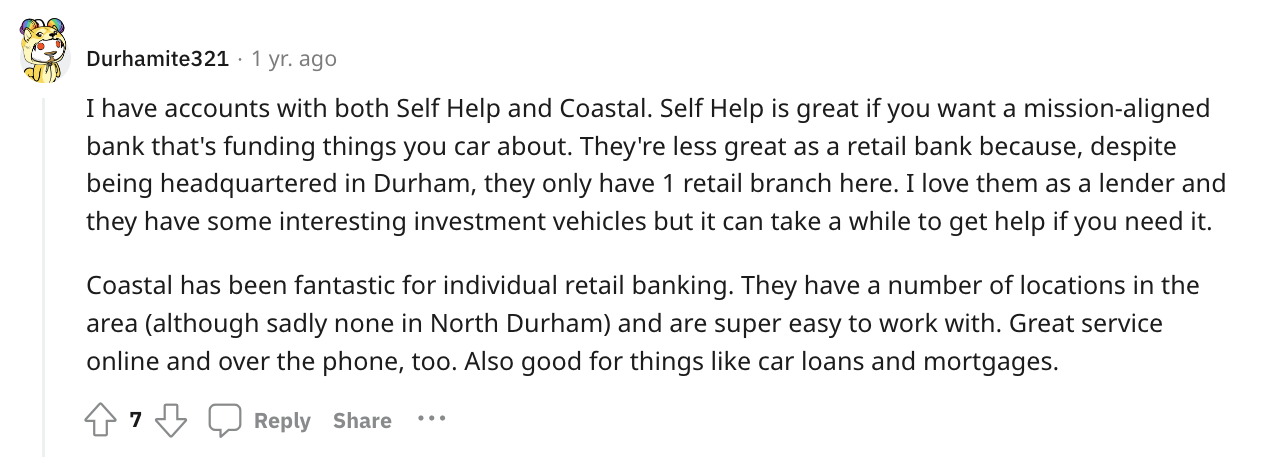

Self-Help is most well-known in North Carolina and California, but has branches spread across 8 states in the United States. And, their offer is super interesting.

Here, I’ll give you the full, uncut picture of what you can expect if you open an account with Self-Help Credit Union or Self-Help Federal Credit Union.

Here’s what’s in store:

- What is Self-Help Credit Union?

- Self Help Consumer Financial Offers

- Frequently Asked Questions

- Final Thoughts: Is Self-Help a Good Institution to Bank With?

Now, let’s get to it!

What is Self-Help Credit Union?

Self-Help is a family of two regional credit unions, a non-profit organization, and an advocacy group. For our purposes, I’ll focus on the banking offers from the two credit unions.

First, Self-Help Credit Union is a financial institution based in Durham, North Carolina, that offers banking products in the United States — More specifically in the following states:

- Florida

- North Carolina

- South Carolina

- Virginia

Right now, Self-Help Credit Union has 37 branches in these states.

Next, Self-Help Federal Credit Union, based in Modesto, California, provides a related offer serving the following states:

- California

- Illinois

- Washington

- Wisconsin

Self-Help Federal has 38 branch locations.

Both offers highlight nationwide surcharge-free ATM access and services at CO-OP shared branches (essentially, you can walk into a partner credit union across the country and make deposits or withdraw funds).

No matter which state you open your account in, you’ll be able to access the same CO-OP shared branches and ATMs – Again, the organizations’ presence is strongest in California and North Carolina.

Self-Help’s mission is to “create and protect ownership and economic opportunity for all, especially people of color, women, rural residents, and low-wealth families and communities.”

To achieve this, they offer fair consumer and small business financial services and lending products with a focus on underserved demographics.

Recommended: Manage Your Money More Efficiently With These 4 Banking Trends

Credit Union vs Bank

Credit Unions and banks offer many of the same financial products (i.e. checking and savings accounts, investment accounts, loans and lines of credit). However, there are some major differences between the two types of institutions.

Credit unions are:

- Owned by members (you and others who use it).

- Non-profit organizations, so they often have lower fees and better interest rates.

- Typically more community-focused and offer a personal touch in service.

Meanwhile, banks are:

- Owned by shareholders or investors.

- For-profit institutions, which can mean higher fees and potentially lower interest rates.

- Probaby offering a broader range of services and may have more branches and ATMs.

In short, credit unions are member-owned, non-profit, and community-oriented, while banks are typically for-profit, with a wider range of services but potentially higher costs.

Recommended: What You Should Consider When Choosing a Bank

Self-Help Company Overview

Self Help Credit Union was founded in 1980 in Durham, North Carolina. Self Help Federal headquartered in Modesto, California, has been around since 2008 (note, there was a major housing crash in the U.S. around this time…coincidence?).

These are not-for-profit, grant-funded financial institutions that collectively serve 183K+ members in the low and middle income range.

With big banks like JP Morgan Chase and Wells Fargo dating back to 1871 and 1952 respectively, Self-Help is a baby in the industry. Sometimes with youth comes new opportunities. And, when you bank with a credit union, you’re not looking for the big bank experience.

Self-Help Eligibility Requirements

So, who qualifies for a Self-Help Credit Union checking account? Some credit unions like Navy Federal or SECU require that you have ties to a veteran or a state employee — This is not the case with Self-Help.

To sign up for a free Self-Help membership, you must either live in a qualifying location or be eligible through your employer. Self Help Credit Union and Self-Help Federal serve many communities and employers in the states where they have branch locations.

If you don’t qualify through your county of residence or employer, you can pay a one-time $5 fee to become a “mission-supportive member.” So, basically, anyone is eligible.

To find out whether or not you can become a free member, reach out via phone to speak with a customer rep during regular business hours:

- Self-Help Credit Union (East Coast): 800-966-7353

- Self-Help Federal Credit Union (West Coast & Illinois): 877-369-2828

Self Help Consumer Financial Offers

As with all financial institutions, Self-Help accounts have their pros and cons. If you’re exploring this offer, chances are you’re uninterested in a big bank offer. And, as with many credit unions, there may be a technology/convenience trade-off.

Let’s find out what financial services you can take advantage of if you become a Self-Help member.

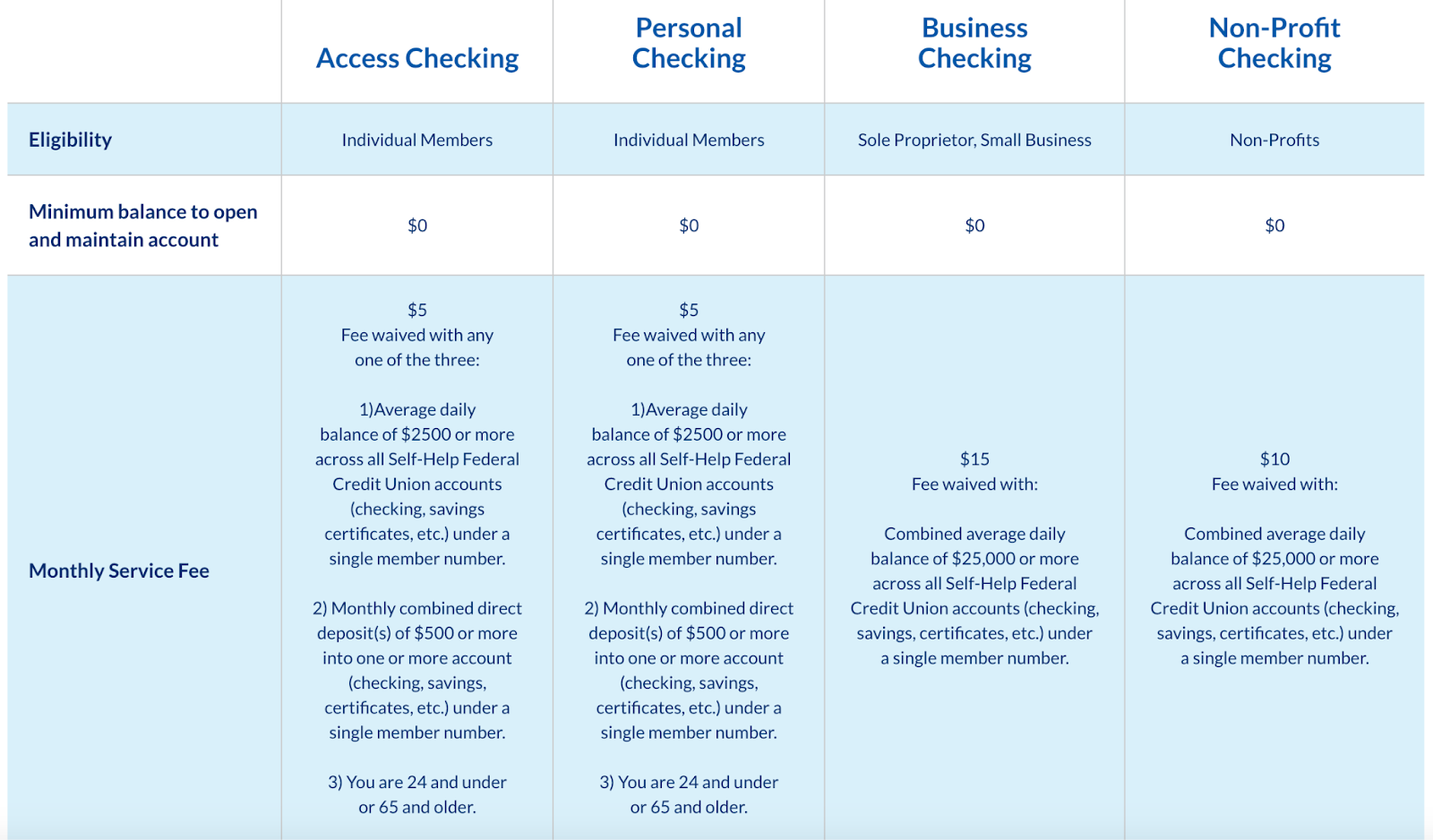

1. Checking & Savings

Self-Help Credit Union, on the East Coast, provides a Personal Checking account with no minimum deposit, a $5 monthly fee (waived under various conditions), and perks like competitive interest rates and free starter checks. They emphasize community focus and member ownership.

Self-Help Federal Credit Union on the West Coast offers a range of checking accounts, including Access Checking and Business Checking, each with a $5-$15 monthly fee (waived under specific conditions). Features include free e-statements, surcharge-free ATMs nationwide, and options for fee reduction based on average daily balances or age eligibility.

Both credit unions provide mobile banking, free ATM/debit cards, and a commitment to passing savings back to members.

Self-Help Credit Union on the East Coast offers a Savings Account with a low minimum deposit of $5, no minimum balance requirement for dividends, and features like competitive interest rates, federal deposit insurance up to $250,000, and convenient online and mobile banking. This account can also be linked to provide overdraft coverage for the Personal Checking account.

Self-Help Federal Credit Union on the West Coast provides a Savings Account with a low $5 minimum deposit, offering above-average dividends on deposits of $100 and above. Notably, this account comes with no monthly service fees, free e-statements, and the option to link it to another Self-Help Federal account for automatic saving. Additionally, customers can enjoy the benefits of free online banking and an ATM card for easy access to their savings.

Recommended: Best High-Yield Checking Accounts That Will Make Money as You Sleep

2. Certificates & Retirement Accounts

Moreover, Self-Help gives members the opportunity to invest in their future with money market accounts, term certificates, and Individual Retirement Accounts (IRAs).

Both Self-Help Credit Union and Self-Help Federal Credit Union offer a range of Term Certificates, providing flexible investment options with competitive dividends. Self-Help’s certificates, available for terms ranging from three months to five years, offer higher rates on longer terms.

And, they are NCUA-insured for added security, with specialized options like the IRA Term Certificate for tax-advantaged savings and the Women & Children Term Certificate supporting empowerment initiatives.

Self-Help Federal emphasizes:

- Attractive dividends

- Guaranteed returns

- NCUA-insured protection

Terms range from three months to five years and a $500 minimum deposit.

Both credit unions encourage local investment with options like the Go Local Term Certificate, and while early withdrawal penalties apply, these certificates can be a smart addition to a diversified savings plan.

Both Self-Help Credit Union and Self-Help Federal Credit Union provide Individual Retirement Accounts (IRAs) with a $500 minimum deposit and the flexibility to add deposits annually. These tax-advantaged retirement savings options offer competitive dividends above standard savings rates and the ability to open a term certificate within the IRA.

With both Traditional and Roth IRA options, account holders benefit from features like no set-up or maintenance fees, the option to deduct contributions (consult your tax advisor), and the choice between tax-deferred dividends (Traditional IRA) or tax-free accumulation and distribution (Roth IRA).

Whether aiming for tax-deductible contributions or tax-free earnings, these IRAs cater to various retirement savings preferences.

Recommended: How to Retire Before 50: 5 Important Habits for Early Retirement

3. Community Recovery Initiative

The Community Recovery Initiative by Self-Help encourages individuals, foundations, nonprofits, and corporations to invest in Community Recovery Term Certificates or other Self-Help accounts.

It provides benefits such as:

- Flexible terms

- Competitive returns

- Guaranteed returns for supporting communities most impacted by COVID-19

Funds generated from the Community Recovery Initiative aid small businesses, nonprofits, neighborhood investments, and home loans, fostering both personal financial growth and community well-being.

This is a good fit for anyone looking to invest with a purpose — It’s especially suitable for those who want to support communities affected by COVID-19 while earning competitive returns on their investments.

Whether you’re interested in Community Recovery Term Certificates for rainy-day funds or longer-term savings, or you prefer the flexibility of traditional Self-Help money market or savings accounts, this initiative caters to a diverse range of investments.

Recommended: Manage Your Money More Efficiently with These 4 New Banking Trends

4. Personal Loans

Self-Help and Self-Help Federal offer a diverse range of loans to meet various financial needs.

- Auto and RV loans provide financing for vehicle purchases, while personal loans offer flexibility for a range of expenses.

- Credit builder loans are designed to help individuals establish or enhance their credit history.

- Immigration loans assist with fees related to immigration processes.

- Dreamer medical school loans are tailored for individuals pursuing medical education under the Dreamer status.

- In North Carolina, families with disabilities can benefit from assistive technology loans, enhancing accessibility and quality of life.

These offerings cater to a wide audience, providing financial solutions for specific needs and circumstances.

Recommended: A Personal Loan vs. Credit Card: Which is Right for You?

5. Credit Cards

Both Self-Help and Self-Help Federal Credit Unions offer credit cards with fair terms and beneficial features.

Self-Help’s card boasts low variable interest rates, online and mobile access, no annual fee, and a share-secured option for building credit — The share-secured credit card is highlighted as an excellent choice for those looking to re-establish credit or open their first credit card.

Self-Help Federal’s Mastercard, similarly, comes with no annual fee, reasonable balance repayment schedules, and worldwide purchasing power through the Mastercard network. The share-secured Mastercard is presented as an attractive option for individuals aiming to rebuild credit or establish their credit history.

Both credit unions provide accessible and secure credit options for various needs and circumstances.

You might also like: The Self Secured Card: Is it Right for You?

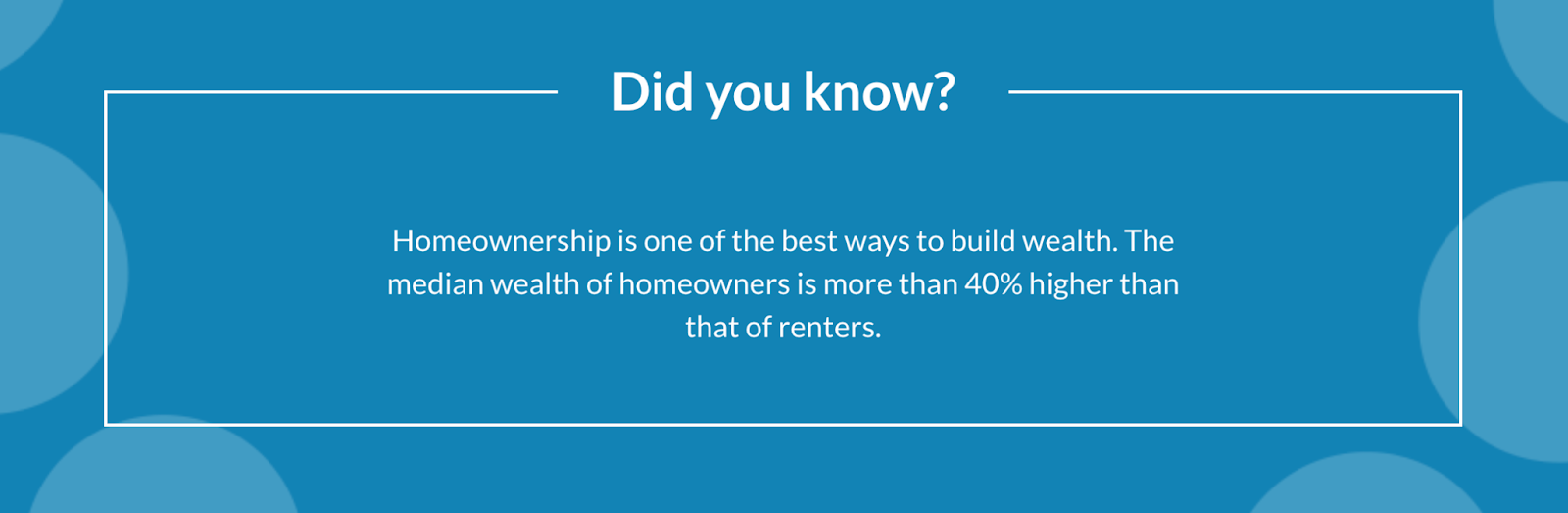

6. Mortgages & HELOCs

Self-Help and Self-Help Federal also offer options for homeownership, catering to those aspiring to buy a home, those seeking pre-qualification, and existing homeowners.

For mortgages, they provide 0% down and flexible mortgage options, allowing individuals to become homeowners with as little as 1% cash to close and credit scores from 580. The absence of private mortgage insurance (PMI) reduces monthly payments.

Additionally, they offer refinancing options, emphasizing the long-term commitment to their clients’ best interests.

On the other hand, Home Equity Lines-of-Credit (HELOCs) from Self-Help Credit Union allow homeowners in certain states to tap into their home’s equity for:

- Large expenses

- Home repairs

- Debt consolidation

With a variable interest rate and terms up to 20 years, this offering provides flexibility for utilizing home equity wealth.

Both mortgage and HELOC options aim to empower individuals on their homeownership journey and leverage home equity for financial needs.

Recommended: This is How to Improve Your Credit Score to Buy a House Fast

7. Financial Education

Both Self-Help and Self-Help Federal Credit Unions offer valuable financial coaching services, providing members with free, one-on-one support to address short- and long-term financial goals.

Members can access financial coaching, with the option for in-branch coaching in select cities.

The coaching involves developing a personalized action plan to:

- Start a savings habit

- Build a strong credit profile

- Pay down debt

- Qualify for loans

In addition to financial coaching, both credit unions partner with GreenPath Financial Wellness, offering a range of free services such as:

- Personal money management support

- Credit report understanding

- Homebuyer counseling

- Foreclosure prevention

- Bankruptcy counseling

- Student loan counseling

- Debt counseling

These services aim to ease financial stress, address concerns, and foster financial health for all members — Self-Help’s comprehensive support system benefits individuals seeking immediate counseling, personalized financial plans, and assistance in various aspects of financial management, making financial wellness accessible.

Frequently Asked Questions

Is Self-Help FDIC Insured?

Self-Help and Self-Help Federal Credit Unions are federally insured through the National Credit Union Administration (NCUA) – not the FDIC – though coverages under both FDIC and NCUA protect deposits up to $250K. Learn more about how NCUA institutions protect your funds.

What credit reporting agency does Self-Help Credit Union use?

Self-Help Credit Union primarily uses Equifax for credit reporting.

What is the limit I can withdraw from Self-Help Credit Union savings?

The withdrawal limit from a Self-Help Credit Union savings account may vary based on the type of account and specific terms. It is advisable to contact the credit union directly to inquire about the withdrawal limits associated with your particular savings account.

Does Self-Help Credit Union lend to those who have filed bankruptcy?

Self-Help Credit Union may consider lending to individuals who have filed for bankruptcy. However, eligibility criteria and terms may vary. It is recommended to consult with the credit union directly to discuss specific circumstances and loan options available.

What does Self-Help Credit Union require for a personal loan?

To obtain a personal loan from Self-Help Credit Union, individuals typically need to provide information such as proof of income, credit history, and details about the purpose of the loan. Specific requirements may vary, and interested applicants should contact the credit union for precise details.

Is there a limit to how much I can deposit to my Self-Help Credit Union personal checking account?

The deposit limits for a personal checking account at Self-Help Credit Union may vary based on the type of account and specific terms. It is recommended to contact the credit union directly to inquire about the deposit limits associated with your particular checking account.

Final Thoughts: Is Self-Help a Good Institution to Bank With?

Alright, let’s cut to the chase on Self-Help Credit Union and Self-Help Federal Credit Union. Based in NC and CA but spread across 8 states, they’re not your average financial institutions – they’re on a mission.

Membership? Easy. Live in the right place or work at the right spot, or just toss in a one-time $5 fee. Boom, you’re in.

What’s in store? Everything from basic checking to dreamer med school loans. Credit cards with low rates, mortgages with 0% down, and a HELOC if you’re into tapping home equity.

But it’s not just about you – they’re big on community impact. The Community Recovery Initiative lets you invest where it matters.

Tech-wise, they’re not the flashiest, but who needs fancy apps when you’ve got free financial coaching and GreenPath on speed dial?

In a nutshell, if you’re into financial diversity, community impact, and a chill vibe, Self-Help is your jam. Just remember, it’s not all high-tech – but hey, who needs frills when you’ve got a credit union with a cause that won’t nickel and dime you to death?

To dive into the world of credit repair and get that credit score up fast so you can move forward with your life, check out Credit Secrets today.

Ashley Kimler

Ashley Kimler is your friendly Credit Secrets wordsmith. With a knack for turning complex money matters into easy-to-digest advice, Ashley has been a trusted voice in the world of finance. With writing credits from Pangea Money Transfer, Centier Bank, Performio, and more, she's here to help you navigate the financial jungle with a dollop of wisdom. Let's turn sense into dollars together!