The Self Secured Credit Card: Is it Right for You?

If you’re trying to build credit, chances are you’ve heard of the Self secured credit card. And, compared to other secured cards, it gets a lot of hype as a means to build or improve credit.

But, is it worth it? — That’s what I’m going to help you figure out.

I’ll tell you what the Self Visa® Secured Credit Card is and explain the difference between secured and unsecured cards. Then, I’ll share a quick overview of the company, along with the parent credit builder offer, and explore the features and benefits of the card.

Here’s what’s in store:

- Secured vs Unsecured Credit Cards

- What is the Self Secured Credit Card?

- Self Secured Card Features & Benefits

- Frequently Asked Questions

- Conclusion: Is the Self Card Worth it?

Now, let’s roll…

Secured vs Unsecured Credit Cards

Alright, so here’s the lowdown on secured and unsecured credit cards.

Think of secured cards as the “try outs” of credit. You front some cash, usually a couple of hundred bucks, which acts as your security deposit and sets your credit limit. It’s like telling the credit authorities, “Hey, look what I can do.”

Unsecured cards, on the other hand, are the cards you get once you’ve made the team. You need no cash upfront (the credit is freely given by the lender) but they’re pickier about who they let in – Your credit history and score need to impress to snag one of these.

Keep in mind that without some practice paying bills on-time, as agreed, any credit card can land you completely ineligible to play. And, secured cards are not the only way to establish credit.

Recommended: Top 8 Best Credit Repair Books of All Time +Free Resources

What is the Self Secured Credit Card?

The Self Visa Secured Credit Card is a tool to boost your credit scores. It’s not your typical credit card—no hard credit check required. Instead, it’s backed by your $100 or more savings progress in a Credit Builder Account, giving you control over your credit limit.

You choose how much of that stash secures your card. Plus, the card reports to major credit bureaus, helping you make a positive credit history splash. It helps you build credit while keeping your hard-earned cash in check.

And, if you make the right moves, it might help you score a credit limit boost over time (this is the main appeal of the offer).

The Self Secured Credit card is not issued by Self Financial, but Lead Bank, which is a trusted, FDIC-insured lender. Originally known as Garden City Bank in 1928, and revamped in 2010 as Lead Bank, this cool community bank delivers classic banking, BaaS (that’s Banking as a Service), and payment solutions.

Now, speaking from experience, credit builder accounts and secured credit cards are not required to build or repair credit. And, they always come at a cost. As you read more, ask yourself if the prices are worthwhile to you.

You might also like: Applying for a Mortgage? How to Prepare Your Credit

Self Secured Credit Card Requirements

To be eligible for the Self Visa Secured Credit Card, you’ll need to meet certain requirements:

- Active Credit Builder account in good standing

- At least 3 consecutive, on-time payments toward your Credit Builder account

- $100 or more in Credit Builder savings (after fees & interest)

- “Stable income”

If you meet these requirements, you’ll have the opportunity to apply for a Self Visa Secured Credit Card using the money from your Credit Builder Account as a security deposit.

Next, I want to share a quick overview of Self Financial and the Credit Builder offer before we dive into the features and benefits of the secured card.

Recommended: Secured vs Unsecured Credit Card: What’s the Difference?

Self Company Overview

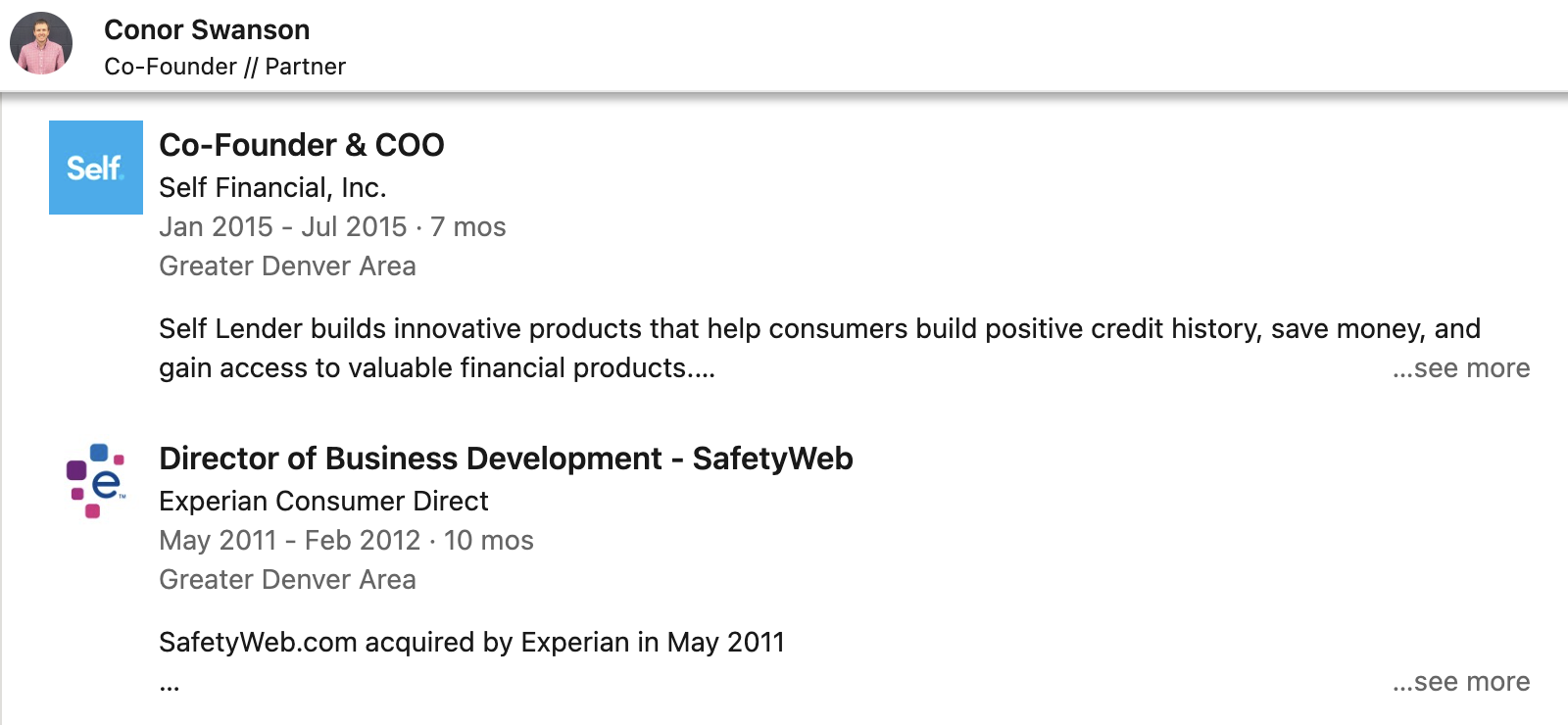

Self Financial, aka Self Inc. or Self Lender is a venture-backed, for-profit, fintech startup that was founded in 2015 by Conor Swanson and James Garvey.

Prior to launching Self, Swanson was the Director of Business Development for Safety Web, which was acquired by Experian while he held this position. He also co-founded LoHi Labs in 2012 and Code Talent Agency in 2014.

Garvey had a couple of entrepreneurial ventures prior to Self as well, though the credit builder offer appears to be his main project at this time. According to Glassdoor reviews, people really like working for Self Financial, which can speak volumes for a company’s credibility.

The leadership seems to be legit and Self Financial appears to be a trustworthy company. So, let’s take a quick look at the main offer.

Self Credit Builder

Self Credit Builder is supposed to be an amazing tool for those looking to level up their credit game. They call it a “loan,” but it’s funded by your own cash.

Here’s the deal: you make monthly payments into a deposit account and it hangs out there until your goal is met. So, it’s actually a savings account that you don’t access until you hit a certain amount.

So, why would you even want to do this when you could use a traditional savings account?

Well, your on-time payments to the so-called “loan” get reported to all three of the major credit bureaus, adding on-time payment history to your credit report. Then, once you’ve paid into the account, you get access to all the cash you’ve stashed.

You will have the option to withdraw funds early from a Self Credit Builder Account, but there are considerations and potential fees associated with early withdrawals. The early withdrawal fee is typically less than $5, depending on the size of your Credit Builder Account.

This isn’t bad, but late payments may incur even more fees — for payments 15 days late or more you might have to pay up to 5% of the scheduled monthly payment.

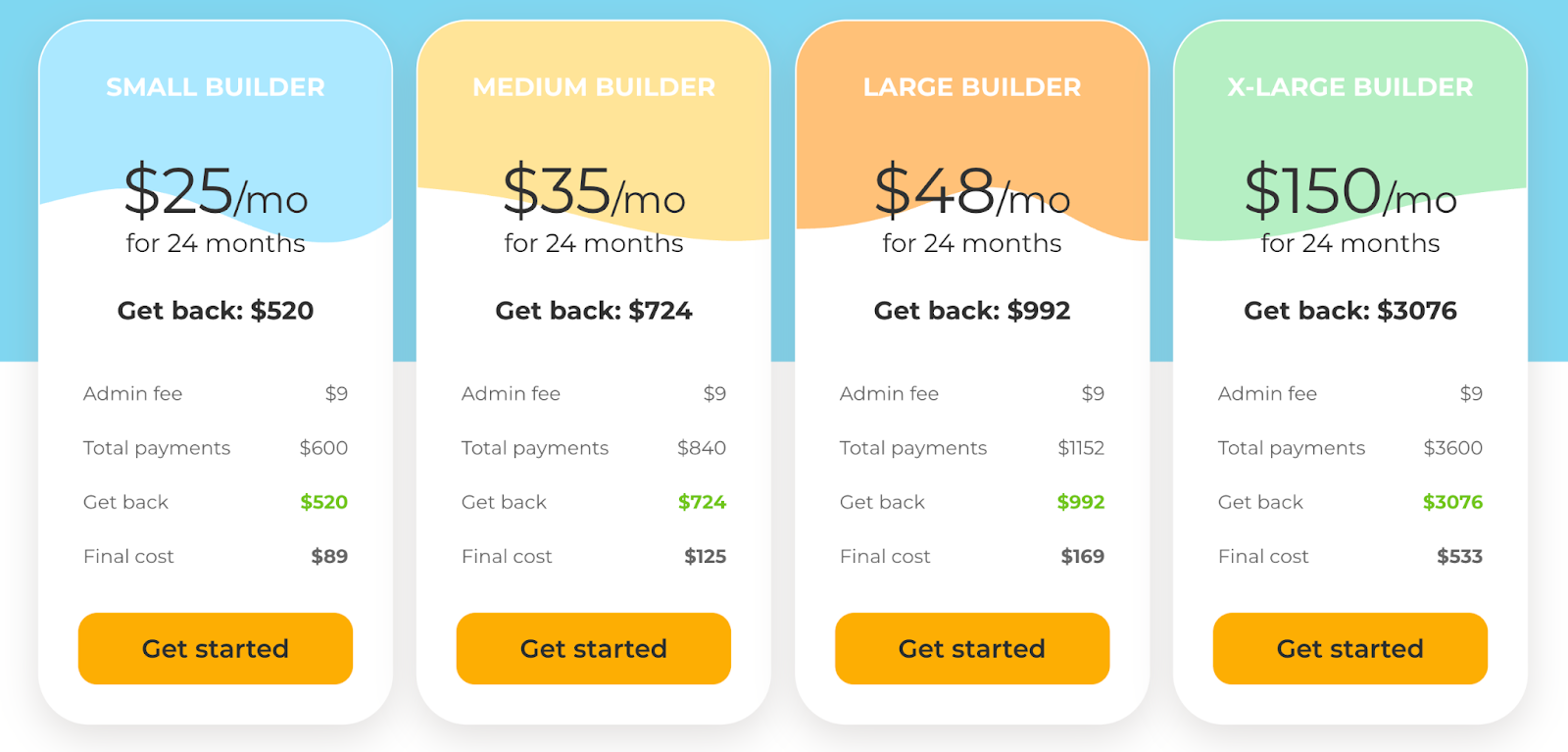

If it helps, think of the Self Credit Builder like a service to report savings efforts to credit bureaus…that costs between $89 and $533, depending on the size of your account and pending you make every payment on time.

Recommended: How Does Self Credit Builder Work? The Big Picture

Self’s Free Rent Reporting

In addition to the Credit Builder offer, the Self Financial website also advertises free rent reporting to all three major credit bureaus. This is a decent offer. And, while I can’t test it for you because I don’t make a rent payment, I would say it’s worth considering.

I won’t dive too deep here, but basically you should be able to connect your bank account, identify the transactions that show your rent payments, and request that Self Financial report these payments to Equifax, Transunion, and Experian for you.

In addition, you can take advantage of a couple other offers:

- Get your cell phone and utility payments reported for $6.95 per month

- Report up to two years of past payment history for $49.95

The price is definitely right, and I see how this could help with your FICO and Vantage scores…Now, whether or not lenders would consider these when making credit determinations, I can’t say.

You might also like: The Free Freeze, Pros and Cons

Self Secured Card Features & Benefits

Now, let’s look at what you came here for: the Self secured credit card offer. Find out if it’s the right credit building tool for ya!

1. No Extra Cash Upfront

What I like most about this offer is that there’s no need for you to fork out extra cash upfront – your secured card account will be funded with the cash in your Credit Builder Account savings (which you would have paid in previously). This means that with this particular secured card, you can piggyback on efforts you’re already making with Self Financial.

While it’s your money that you’re spending (the card is never funded by a lender), this card does offer a convenient way to access the money you’re putting in. And technically, it could help you bypass any early withdrawal fees.

But, there are other fees…

Recommended: DIY Credit Repair Demystified (It’s Not as Hard as You Think)

2. Competitive Annual Fee & APR

Self’s annual fee is $25, though it may have been higher in the past. This cost is competitive with other similar offers (this can range from $19 to $36 on trusted, popular secured card offers like those from OpenSky and Merrick Bank).

Now, Self’s current (variable) APR for the secured card — which is not the same as their APR for the credit builder “loan” — is 29.24%. Competitors tend to charge just 22% variable APR. So, Self is a little high in this respect.

However, you don’t ever have to pay interest fees if you pay your balance in full each month.

3. Spend Anywhere Visa is Accepted

One definite perk is that this secured card is a Visa card, which can be accepted pretty much anywhere. This isn’t a standout feature, as many secured cards are issued by either Visa or Mastercard. Still, it’s an important feature to look for in a secured card.

The last thing you want is to have your money tied up in a fund that you can’t spend where you need it.

4. Low Minimum Credit Limit

To my knowledge and from what I’ve observed, the minimum credit limit on secured credit cards is typically $200 to $300 – This is because the lenders need to make the offer worthwhile. It takes effort (even with automated systems) to set up accounts and hand out credit cards.

With Self Financial’s current business model, they’re able to hand out secured credit cards with a limits as low as $100 – this could be super nice for someone with low income or limited investment in their Credit Builder account.

Frequently Asked Questions

How does the Self Credit Card work?

To get started, you need an open, active Self Credit Builder Account. If you meet the eligibility criteria, you can apply for the Self Visa Secured Credit Card. The card is funded with the savings in your Credit Builder Account, which enables you to set your spending limit. On-time payments are reported to Equifax, Transunion, and Experian.

Does Self Credit do a hard pull?

No, there’s no hard credit check when applying for the Self Credit Card. It’s a secured credit card, so the focus is on meeting Self Financial’s eligibility requirements based on Self Credit Builder account activity.

What is the max limit on the Self Credit Card?

The maximum credit limit on the Self Credit Card is flexible and depends on the savings progress in your Credit Builder Account. You choose what portion of your savings (with a minimum of $100) will secure your card and determine your own limit.

Does the Self Credit Card become unsecured?

The Self Credit Card starts as a secured card, but over time, with responsible use and keeping your account in good standing for at least six months, there may be an opportunity to transition to an unsecured credit card.

Can I use my Self card to rent a car?

Yes, you can use your Self Credit Card to rent a car. The Self Visa Credit Card can be used wherever Visa credit cards are accepted in the U.S., including car rental agencies. Keep in mind that individual rental car companies may have specific policies and requirements, so it’s a good idea to check with the rental agency beforehand to ensure a smooth transaction.

Conclusion: Is the Self Card Worth it?

The Self Secured Credit Card works a bit like a debit card and is funded from your Self Credit Builder account, not from borrowed money. While it’s connected to your own funds, using it might mean spending your Credit Builder “loan” early, which could go against your financial goals.

On the positive side, it lets you access your money without penalties, and it adds another account to your credit history.

But, you need to weigh the $49 annual fee against the benefits — If you’re regularly putting money into your Self builder account and need the positive credit impact, it can be a good option. Ask yourself, “Is the annual fee worth it?” and “Can I make on-time payments to boost my credit?”

If you’re not already with Self, think twice, as having secured accounts isn’t the only way to build credit, and a new payment might not help if you’re already struggling.

To dive into the world of credit repair and get that credit score up fast so you can move forward with your life, check out Credit Secrets and start your journey to better financial health.

Ashley Kimler

Ashley Kimler is your friendly Credit Secrets wordsmith. With a knack for turning complex money matters into easy-to-digest advice, Ashley has been a trusted voice in the world of finance. With writing credits from Pangea Money Transfer, Centier Bank, Performio, and more, she's here to help you navigate the financial jungle with a dollop of wisdom. Let's turn sense into dollars together!