How Does Self Credit Builder Work? The Big Picture

Recently, we did a write up on the Self Secured Credit Card, which is part of the Self Credit Builder offer. For the most part, I liked the card (for some groups). So, I wanted to delve a bit deeper into the bigger offer and explain how Self Credit Builder works…This is what I came up with.

Here, I break down the ins and outs to explain the offer in detail, and who it might be a good fit for. Then, I answer some of the top questions people have about this offer and help you decide – once and for all – if you should sign up.

Here’s what’s in store:

- What is Self Credit Builder?

- How Does Self Credit Builder Really Work?

- Supplemental Credit Building Offers From Self

- Frequently Asked Questions

- Conclusion: Should You Sign Up?

Now, let’s dive in!

What is Self Credit Builder?

If you’re looking for a way to build credit so that you can make a major purchase, you might come across this offer. So, what is it?

Self Credit Builder is a service from Self Inc., focused on improving credit scores by reporting rent payments to all three major credit bureaus within 72 hours. It requires no credit card or check, and the application process does not involve a hard credit pull.

The system offers an autopay feature for convenience and enables users to track their credit scores over time at no extra cost. Seems cool, right?

The process involves:

- Applying for a Credit Builder Account

- Choosing a payment plan

- Making on-time monthly payments to build positive credit history

After completing the payment term, users gain access to their savings. Four plans with different monthly amounts and payback structures are available.

Additionally, users can qualify for the Self Visa Credit Card in as little as three months of on-time payments to Self Credit Builder without a hard credit pull.

Now, let’s dig in deep to find out if this offer is all it’s cracked up to be.

Self Company Overview

We’ve covered this before when reviewing the secured card offer, but let’s see a quick overview of the company behind the offer.

Self Financial, also known as Self Inc. or Self Lender, stands out as a venture-backed fintech startup in the for-profit sector. Established in 2015 by Conor Swanson and James Garvey, the company has garnered attention for its innovative credit-building approach.

Swanson, the co-founder, previously served as the Director of Business Development for Safety Web, a company later acquired by Experian. Before the inception of Self, he co-founded LoHi Labs in 2012 and Code Talent Agency in 2014, showcasing a rich background in the industry.

Garvey, the other co-founder, brings entrepreneurial experience to the table, with credit building emerging as a focal point of his recent endeavors.

Glassdoor reviews underscore the positive work environment at Self Financial, shedding light on the company’s credibility – The leadership team appears reputable, contributing to the perception of Self Financial as a trustworthy entity.

In evaluating the primary offering, it becomes evident that Self Financial has positioned itself as a credible and innovative player in the fintech landscape. In sum, as long as you understand what you’re getting into, you can probably trust these guys with your money.

So, let’s see how much you can expect to give Self – in exchange for a chance to build credit – if you enroll. Before that, let’s make sure you know exactly what you’re buying.

How Does Self Credit Builder Really Work?

A Self Credit Builder “Loan” is not actually a loan at all. The way I see it, It’s more like a costly savings account with a twist – they report your on-time payments to credit bureaus.

You apply, set aside money (let’s say $800), and make monthly payments over the course of 6 to 24 months. All the while, your contributions are reported to Transunion, Equifax, and Experian.

The catch? You only get the money after you fully fund your account – compared to a traditional or high-yield savings account, this is a potential downside. However, if you don’t have great spending impulse control, the barrier could be a good thing.

The idea with Self is that your consistent payments, as they are reported to credit bureaus, can potentially boost your credit score.

While Self highlights testimonials of raised credit scores (right now, the predominant testimonial on the website talks about a credit score boost of 70 points), it’s important to always read the fine print.

As Self themselves admits in an article from 2021, the average credit score improvement is 32 points. This is definitely enough, in many cases, to push a credit score from very poor to fair, or fair to good. So, 32 points may have value, but you don’t want to set your expectations too high.

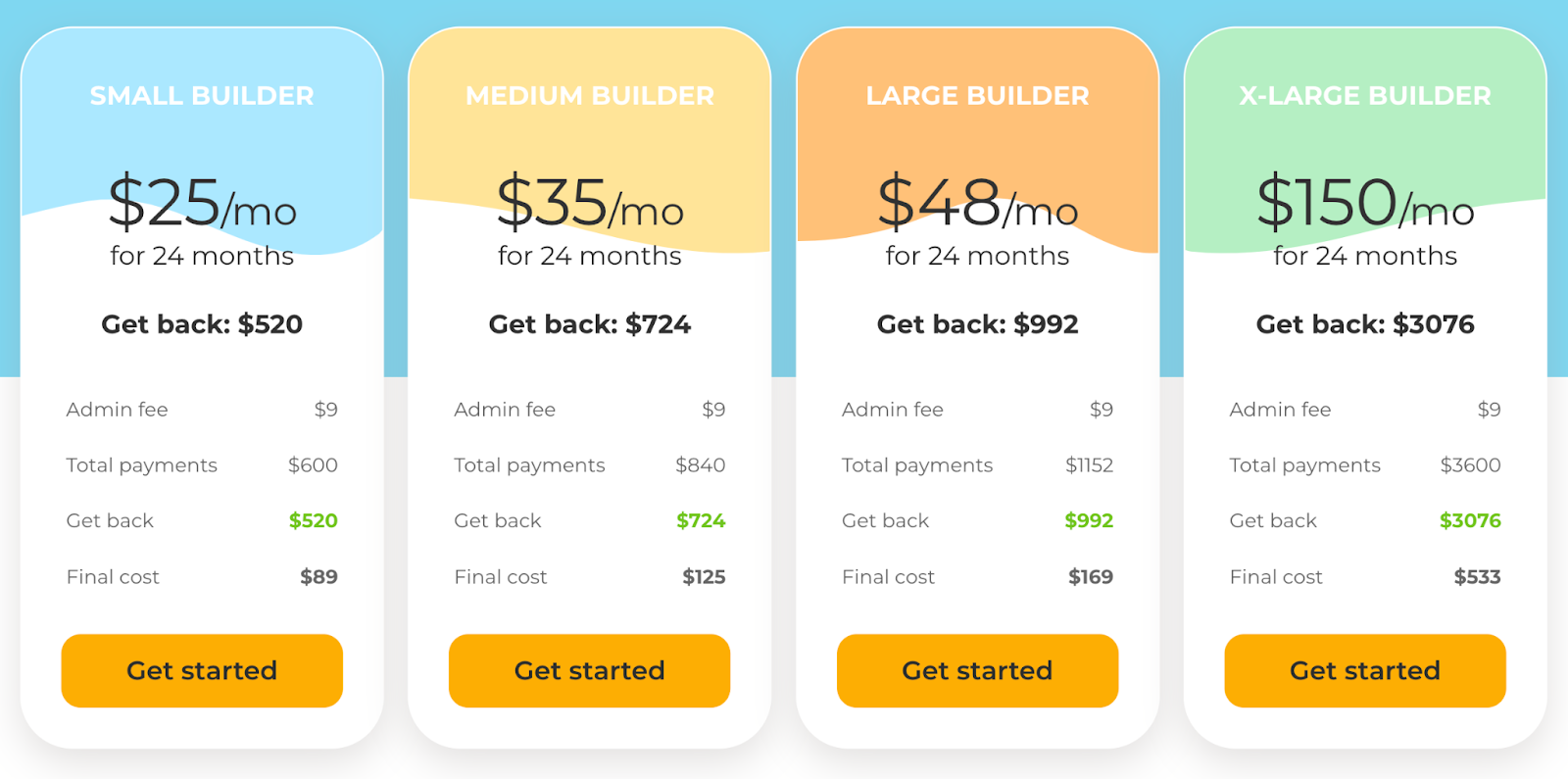

Self Credit Builder Costs Explained

Now, you know about the $9 fee, the interest rate, and late payment fees. Let’s have a look at what these percentages mean, in cold, hard numbers.

Costs include:

- Administrative fees (around $9)

- An interest rate (14% to 16%)

- Early withdrawal fee (less than $1)

- Late payment fees (5%)

Compared to traditional loans, it’s a unique offer – holding your funds until payments are done while helping with credit-building.

(Quick note: I really like that Self is so transparent about costs – this isn’t always the case with financial offers, and especially those designed for credit improvement.)

Here’s the breakdown:

- For $25 per month over the course of 24 months, you will pay in a total of $600 and receive $520.

- For $35 per month over the same time span, you will pay a total of $840 and get back $724.

- For $48 per month, you’ll pay in $1,152 and cash out $992.

- For 150 per month, you’ll pay $3.6K and get $3,076.

So, with perfect payments, you’ll contribute $89 to $553, plus a one-time administrative fee of $9 – Up to $562 total.

As yourself, ‘Is a 32+ point credit score increase worth $562 to me over the course of the next two years?’

If the answer is yes, keep reading!..If not, pick up a book on credit repair (or reach out to a financial professional) and start educating yourself about your options.

Now, you also need to consider how responsible you are with your money because 5% late fees aren’t inconsequential; this is particularly true if your income isn’t the highest.

A 5% late fee on a $3.6K loan is $180! And, for a $600 loan, 5% is $30. A late fee for a missed payment on a Self Builder account could be more than the agreed monthly payment.

However, if you make payments on-time, which is #1 for good credit, you won’t have to worry about late fees. Plus, there are ways to cancel your account and cash out early (for another small fee).

Note, comparable credit builder accounts are available at many banks and credit unions.

Chances are, there is an offer available at the financial institution where you already have a checking and/or savings account. So, it wouldn’t be a bad idea to reach out and see what their options are. It’s always a good idea to shop around, because the worst thing that can happen is that the offer in front of you is the best fit for your needs.

You might also like: This is How to Improve Your Credit Score Fast to Buy a House

Supplemental Credit Building Offers From Self

The Credit Builder “Loan” from Self is only one of their offers. And, while its definitely the meat and potatoes, you can get even more when you open an account with Self. Let’s take a closer look at what they’re selling (through objective eyes).

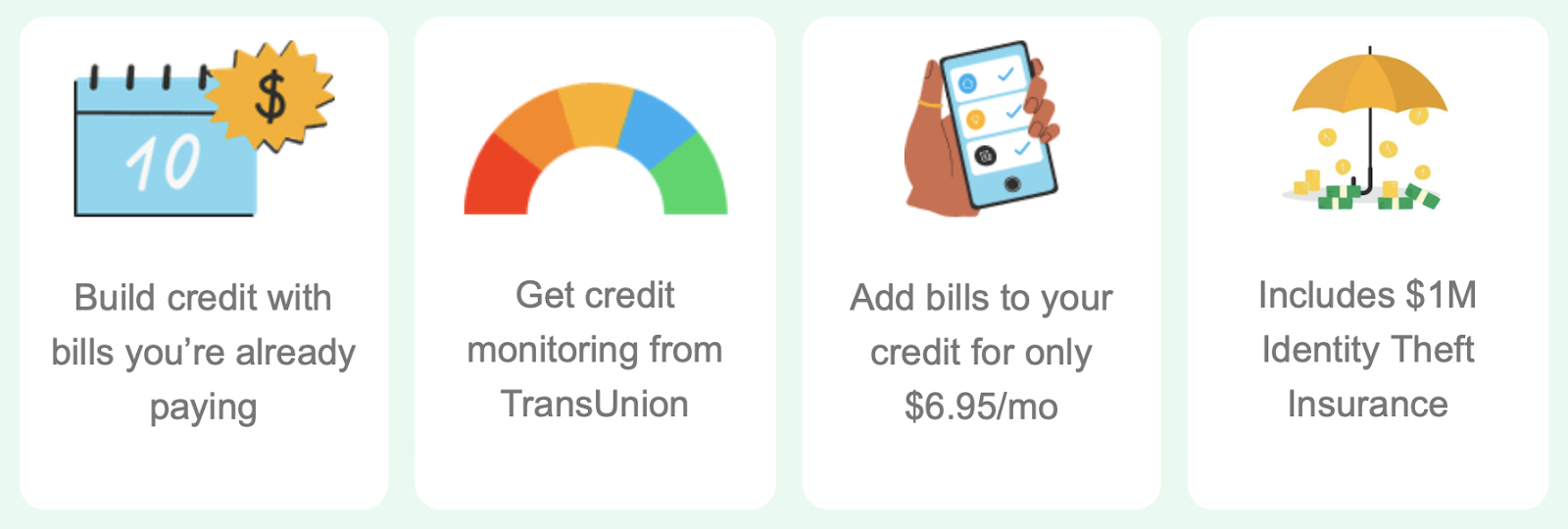

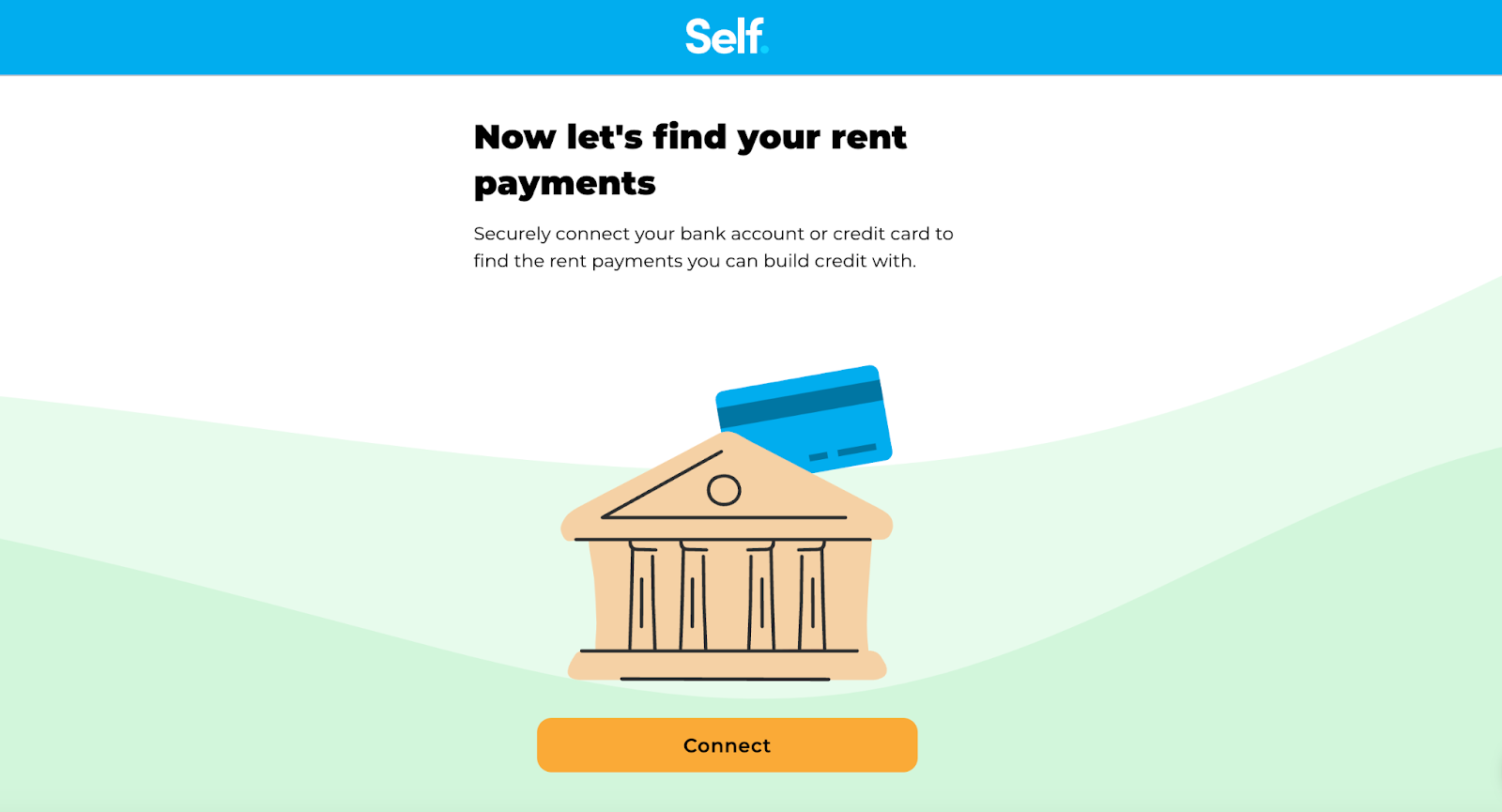

1. Free Rent Reporting

All you have to do is sign up for an account and share your identifying information – your social security number and access to your bank account included. In exchange, Self can report your rent payments to credit bureaus.

Of course, if you have a mortgage, rent reporting isn’t a good fit, as these payments should already be reporting. This offer is only for renters.

Through Plaid, Self will connect to your bank account and find out which transactions were used to pay your rent.

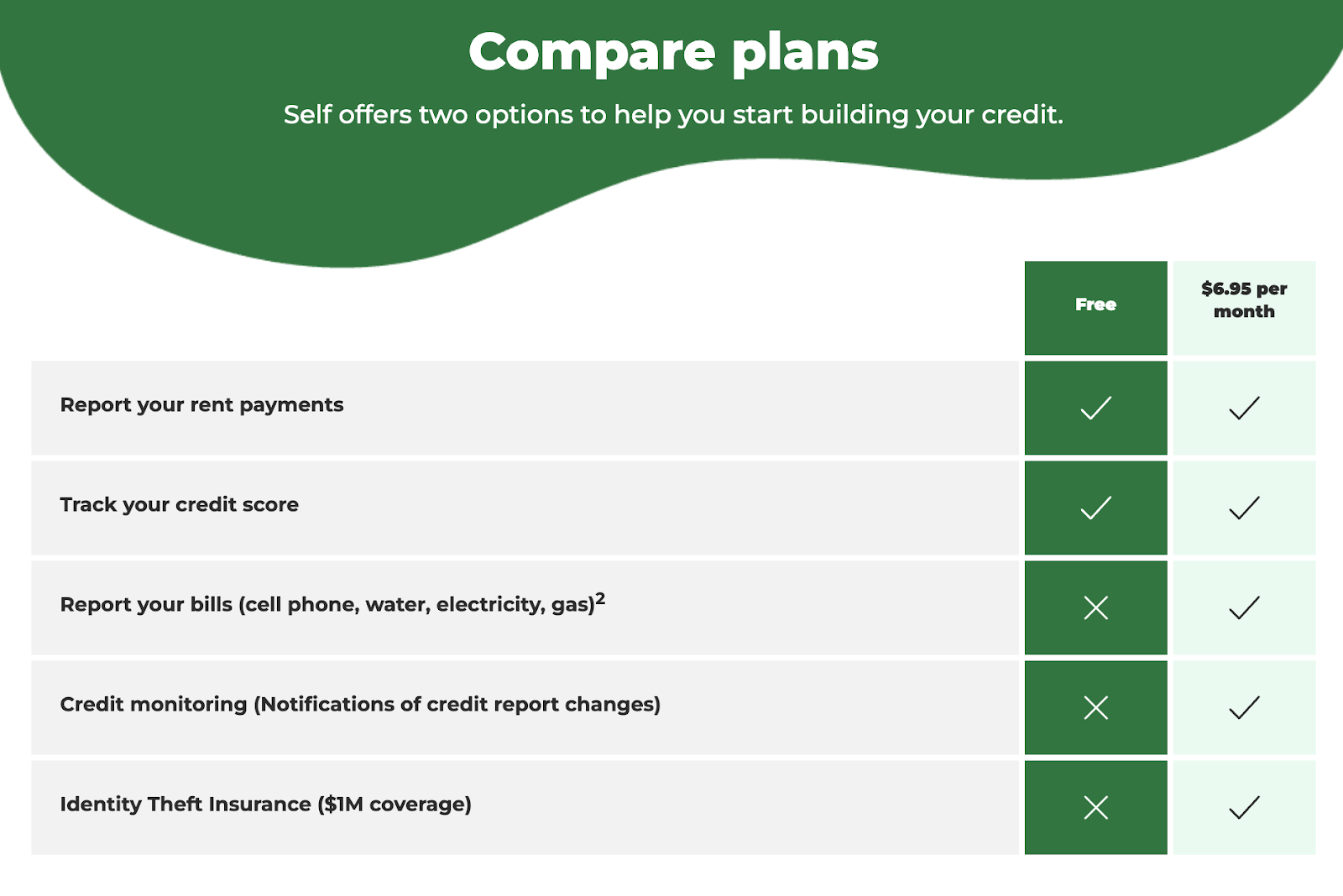

For $49.95, you can get up to 24 months of PAST rent reported – this is only worthwhile if your payments were made from the checking account that you connect and that Plaid is able to find the transactions. This “lookback fee” will only ever be charged one time, even if you choose to upgrade your account in the future.

And, for $6.95 per month, you can upgrade to report other bills and utilities (The premium account is called Rent+Bills).

Recommended: Renting with Bad Credit: Tips & Strategies

2. Low-Cost Bills & Utility Reporting

When you upgrade to a premium Rent+Bills account, you’ll get access to a few added services:

- Cell phone, water, electricity, and gas payment reporting

- Credit monitoring

- Identity theft coverage

For less than $7 per month, this is a low-risk offer that appears to have some potential worth.

Again, always read the fine print. According to Self, this offer has garnered positive outcomes for people who started with a reporting score of 300 to 600. So, anyone currently sitting above that range probably isn’t likely to see results,

And, if you have negative items on your account, rent and utility payment reporting will not help you clean them up.

You might also like: The Truth Behind the “Pay to Delete” Letter

3. Credit Monitoring

With a Rent+Bills account, you also gain access to credit monitoring. What that means is that you can see when new inquiries and changes occur on your credit reports.

While this is a nice bonus, you can get more robust reporting from providers like Credit Karma for free.

Moving on…

4. $1 Million Identity Theft Coverage

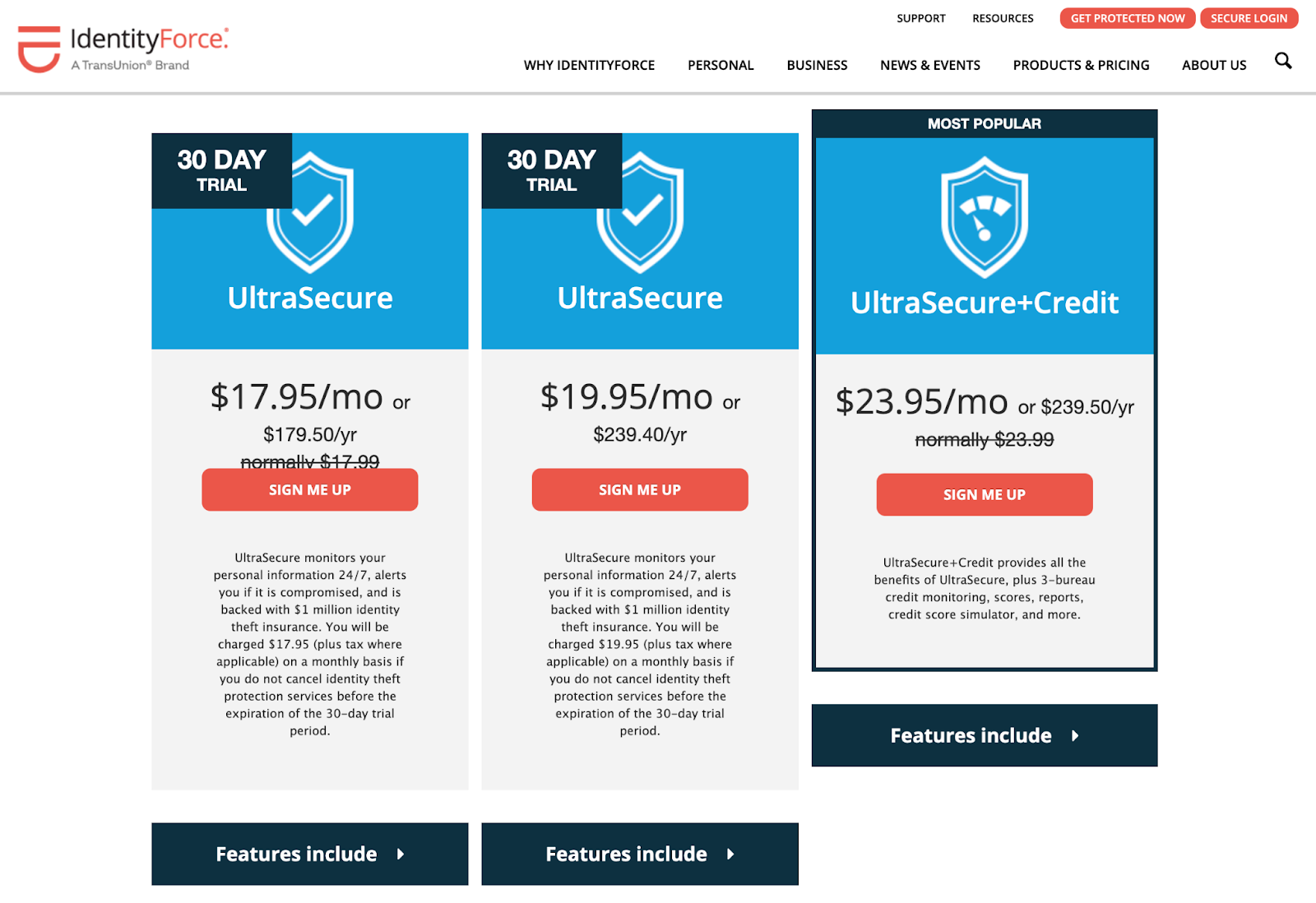

When I first saw that ID theft coverage was covered under the $6.95 per month to upgrade to a premium Rent+Bills account, I thought, ‘That seems like a great deal for insurance,’ and, ‘If I didn’t already have coverage, this insurance might be worth signing up for, even if I don’t use the reporting offer.’

(I know pricing for LifeLock by Norton starts at $7.50 per month.)

But, of course, I had to dig deeper to see what the going rate is, and I found that Nationwide insurance offers a $1 million policy for less than $4 per month – So, while this is a competitive rate for insurance, it wouldn’t necessarily be the very best way to protect your identity.

However, as an add-on to rent reporting, it’s definitely a nice supplemental service.

And, after some digging, I found that the ID theft coverage provided through Self is offered in partnership with IdentityForce. To sign up for an individual account, you would pay at least $17.95 per month.

So, through Self, you might be able to save on identity protection – as long as your premium Rent+Bills account is active.

You might also like: Can IdentityIQ Really Protect Your Finances? The Truth

5. Self Secured Credit Card

The Self Secured Credit Card operates quite a bit like a debit card – you draw funds from your Self Credit Builder account rather than borrowed money. Then, your on-time payments are reported to credit bureaus to help establish more payment history.

While this card utilizes your own funds, using it may deplete your Credit Builder “loan” prematurely – this could throw a wrench in your financial goals.

On a positive note, it provides penalty-free access to your money and contributes to diversifying your credit history. However, your decision to apply for this secured card should factor in the $49 annual fee versus the benefits.

You might also like: Secured vs Unsecured Card: What’s the Difference?

If you consistently contribute to your Self builder account and you’re looking for a positive credit impact, it can be a viable choice. Consider the annual fee and your ability to make timely payments when deciding if this card is right for you.

For anyone not currently with Self, I advise you to take a step back and think hard before you apply – Secured accounts aren’t the only way to build credit, and introducing a new obligation to your monthly budget might not be the next best step to take.

Recommended: The Self Secured Credit Card: Is it Right for You?

Frequently Asked Questions

Do you get all your money back from Self Credit Builder?

No. With a Self Credit Builder Loan, you will pay in more than you can withdraw at the end.

What are the downsides of a Self Credit Builder?

There are costs (up to $562) associated with Self Credit Builder products, and there is no guarantee that it will increase your credit score.

How fast does Self improve credit?

With Self, you could see a credit score improvement as soon as they report your first payment to credit bureaus, in as few as 30 days. However, there are no guarantees that your credit score will improve at all.

Can I pay off my self loan early?

Yes, you can pay your self loan off at any time, and there is no early payment penalty.

What happens when you complete a Self Credit Builder?

When you finalize payment on a Self Credit Builder Loan, you may withdraw or spend your funds. Alternatively, you could apply the funds toward a Self Secured Credit Card account.

Conclusion: Should You Sign Up?

What I love about Self’s offer is that the pricing and other pertinent information are super transparent. So, it’s pretty easy to know what you’re getting into before you sign up. On the front end, they aren’t so clear about the ID theft coverage. But, that is probably due to their agreement with IdentityForce, so I wouldn’t knock them for it.

Self is a legitimate company that has a lot invested into helping people raise their credit scores. And, for some people, it really works! — Some folks go through the program and absolutely love it.

For others, the investment isn’t worth the results. In all, it can cost up to $562 (not including a Rent+Bills upgrade, late fees, or costs associated with a Self Secured Credit Card) and 24+ months of your life for a gamble at boosting your credit score.

Unfortunately, there’s no magic pill that works for everyone, and Self is not a good fit for those who don’t want to invest that much time or money…

…It is not a great fit for anyone whose credit score is 600 or above…

…Nor is it going to fix credit with poor payment history or complex credit issues. For those, you’ll need a more bespoke approach.

To dive into the world of credit repair and get that credit score up fast so you can move forward with your life, check out Credit Secrets and start your journey to better financial health.

Ashley Kimler

Ashley Kimler is your friendly Credit Secrets wordsmith. With a knack for turning complex money matters into easy-to-digest advice, Ashley has been a trusted voice in the world of finance. With writing credits from Pangea Money Transfer, Centier Bank, Performio, and more, she's here to help you navigate the financial jungle with a dollop of wisdom. Let's turn sense into dollars together!