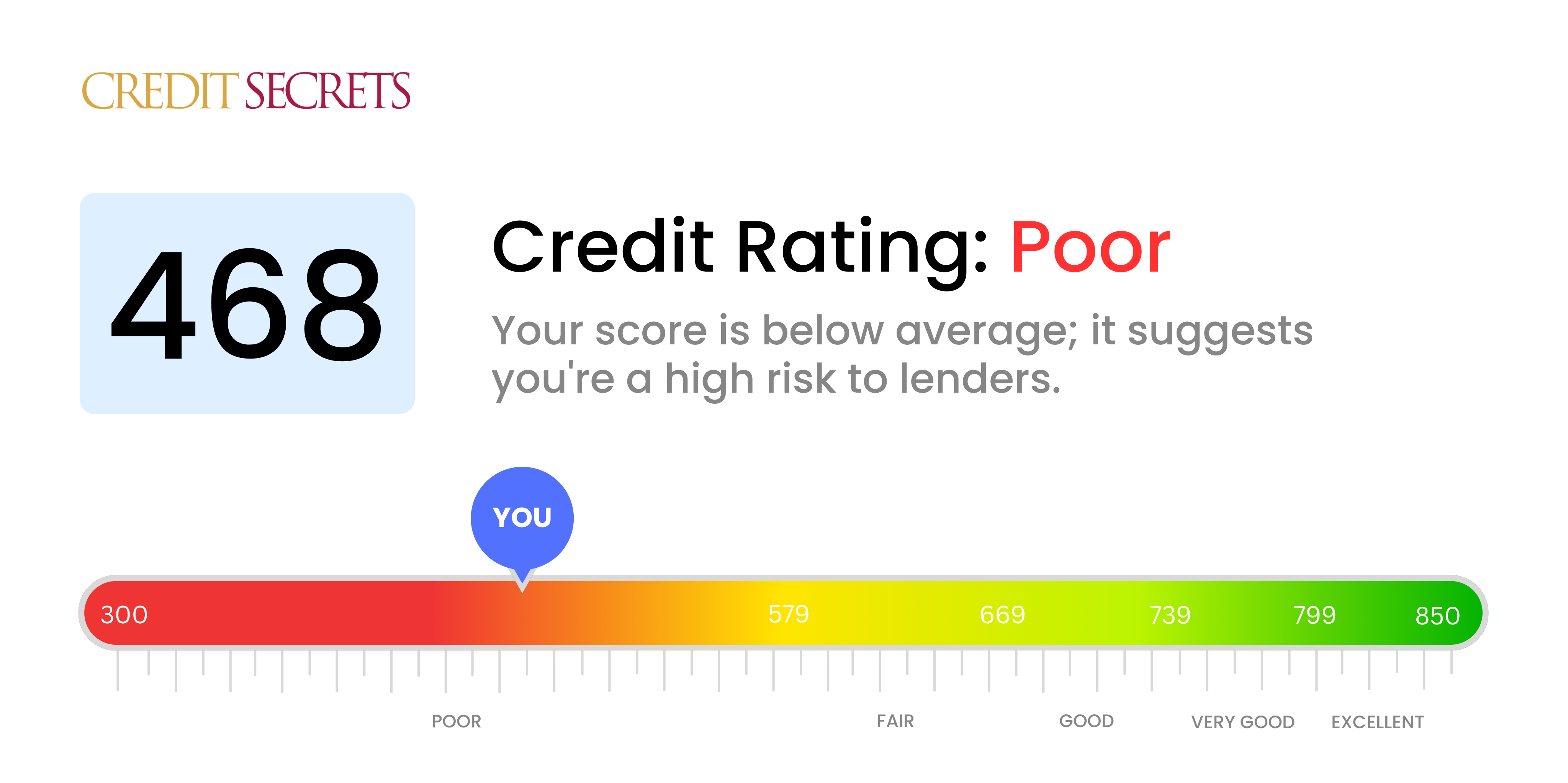

Is 468 a good credit score?

With a credit score of 468, it's clear that you're currently facing some financial hardships, as this falls in the 'Poor' category. This doesn't mean you're stuck, though - there are many ways to uplift your score and bolster your financial stability. While it might be harder to secure loans and better interest rates now, by taking proactive measures, you can substantially improve your score.

Unfortunately, with this credit score, you'll likely encounter some challenges when trying to get approved for credit cards, mortgages, auto loans, or personal loans. However, remember that a credit score is only a snapshot of your financial status at this given time—it's well within your control to turn the tables to your favour. Follow sound financial practices, pay off debts timely, and strive to maintain financial discipline, and you'll slowly see your score improve. Be patient, as this takes time, but every step you take brings you closer to a healthier financial future.

Can I Get a Mortgage with a 468 Credit Score?

A credit score of 468, unfortunately, indicates a significantly lower-than-average credit rating. More than likely, this score will not meet the requirements necessary to be approved for a mortgage. This score reflects a substantial amount of financial struggle, possibly due to delayed payments or defaulting on past credits. This is not an easy situation, but please know you are not alone.

One possible course of action is to explore alternative lending options. An FHA loan, for instance, caters to those with lower credit scores. However, keep in mind that even with an FHA loan, borrowers typically need a minimum score of 500. Approval based on a lower score can be subject to a larger down payment. Your focus should be aimed towards improving your credit score, practicing disciplined spending, and maintaining a stable payment history. Believing in yourself is key, and remember, rebuilding your credit isn't impossible—it will just take time and effort.

Can I Get a Credit Card with a 468 Credit Score?

A credit score of 468 often suggests potential difficulty when applying for a traditional credit card. This score might be seen as problematic by lenders, indicating past fiscal problems or mismanagement. It's necessary to understand this predicament with a sense of realism and positivity, remembering that knowledge about one's credit is an important first step towards financial recovery.

This low credit score might seem like a setback, yet there are practical alternatives available. Secured credit cards, for instance, which necessitate a deposit that serves as your credit limit, could be an attainable option. They can help slowly but surely rebuild one's credit. Another possible course of action could include seeking a co-signer for a loan or making use of prepaid debit cards. It's crucial to understand that these options won't provide an immediate solution, but they can aid in the gradual journey towards a more solid financial foundation. Be aware that interest rates on credit available with a score like this are usually considerably higher, due to lenders view of a high-risk nature.

The credit score of 453 presents a challenging scenario when applying for traditional personal loans. This score is below the generally acceptable range and typically indicates a high-risk borrower. Consequently, most traditional lenders may not be inclined to approve loan applications with this score. It's a tough fact, but it's necessary to recognize the implications of this score on your borrowing opportunities.

It's not entirely a dead-end. Other avenues could be explored. Secured loans, which require collateral, or co-signed loans, wherein someone with a higher credit score backs your application, can be feasible options for you. Alternatively, peer-to-peer lending platforms sometimes offer a comparatively lenient check on credit scores. Yet, it's vital to remember that these alternatives generally come with higher interest rates and less-than-ideal terms, mirroring the increased risk undertaken by the lender.

Can I Get a Car Loan with a 468 Credit Score?

With a credit score of 468, getting a car loan could be quite challenging. Most lenders prefer scores around 660 or higher for the best loan terms. Unfortunately, a credit score that falls below 600 is generally seen as subprime. Your 468 score is within this subprime range, which often translates to more expensive interest rates or the possibility of loan refusal. This is because lenders view a lower credit score as a sign of higher risk, suggesting potential obstacles in paying back the borrowed money.

Despite this, a low credit score doesn't completely diminish your ability to secure a car loan. There are lenders who cater to those with lower credit scores. But it's important to be careful, these loans often come with considerably higher interest rates. This is a measure taken by lenders to mitigate the perceived risk. It might feel like a rocky road ahead, but with diligent consideration of the terms, getting a car loan could still be attainable.

What Factors Most Impact a 468 Credit Score?

Decoding your credit score of 468 is key to building a sound financial future. Let's delve into the components that impact your score and learn how to boost it.

Credit Payment Timelines

Delays or missed payments can affect your score significantly. Such flaws in your payment history might be the reason for a 468 score.

What to do: Scan your credit report to identify any delayed or missed payments and work towards prompt payments in future.

Ratio of Credit Usage

Your credit score can lower if you frequently max out your cards. Possibly, this high credit utilization is one of the causes of your existing score.

What to do: Go through your credit card bills. Are you frequently hitting your card limit? If yes, aim to keep your balance low.

Credit History Duration

A shorter credit history could explain your score. Lack of sufficient credit data can lead to a lower score.

What to do: Inspect your credit report, check the age of your oldest and newest credit accounts. Frequently opening new accounts can affect your score too.

Diversity of Credit and New Credit Management

Having a range of credit like, credit cards, retail accounts, mortgage loans, and installing loans, can strengthen your credit profile. This balance might be missing in your case.

What to do: Analyze your variety of credit accounts. Keep a check on the frequency of your new credit applications.

Public Record Entries

Entries like bankruptcy, tax liens, or collections can impact your score negatively. Possibly, such public records might be influencing your credit score.

What to do: Review your credit report for any public record entries. Address and resolve any listed items.

How Do I Improve my 468 Credit Score?

With a credit score of 468, while currently on the low side, it certainly isn’t fixed. You can take immediate action to improve your score using targeted strategies. Given your current circumstance, here are the most effective steps you can focus on:

1. Review Your Credit Report

Start by getting a copy of your credit report to identify potential errors. Incorrect information can greatly damage your credit score. If you find inaccuracies, dispute them with the relevant credit bureau.

2. Prioritize Outstanding Debts

Paying your bills on time is crucial. Make a list of all your current debts, and focus on paying off the ones that are most overdue. Even a few months of timely payments can start to visibly boost your credit score.

3. Utilize a Secured Credit Card

At this stage, a secured credit card might be the best tool to help rebuild your credit. The deposit you make acts as your credit limit. By making timely payments, you have a chance to increase your credit score substantially.

4. Limit Your Credit Applications

Every time you apply for a loan or a credit card, an inquiry appears on your credit report. This can hurt your credit score further. It’s best to limit new credit applications and focus on nurturing your existing accounts.

5. Establish a Diverse Credit Profile

Once you are on the path to recovery with a secured card, explore other credit avenues. A mix of installment and revolving credit could contribute to lifting your credit score. Just remember, managing these responsibly is key.