Before You Call Lexington Law, Read This Full Review

Lexington Law is one of the most popular legal firms to offer credit repair services in the United States. As with all financial offers, there are pros and cons. And, you need to know what you’re getting into before you call Lexington Law (or any other credit repair service, for that matter).

Here, I’m going to explain what Lexington Law is, give a company overview, and explain what they do. Then, I’ll share some alternatives for you to consider and answer some of the most common questions people are asking.

By the end, you’ll know whether this is the right offer for you or if you should seek another service or walk the DIY credit repair path.

This is what’s in store:

- What is Lexington Law?

- Lexington Law Service Features & Benefits

- Alternatives to Lexington Law for Credit Repair

- Frequently Asked Questions

- Final Thoughts: Is Lexington Law Legit for Credit Repair?

Now, let’s roll!

What is Lexington Law?

Lexington Law is a credit repair service that assists people with the identification and resolution of inaccurate, unfair, or unverified negative items on their credit reports.

Through a lawyer-driven process, Lexington Law follows a three-step approach:

- Review

- Repair

- Restore

The review phase involves a detailed credit report assessment to pinpoint questionable negative items. In the repair stage, Lexington Law engages with credit bureaus and creditors to validate the accuracy and fairness of these items – If discrepancies are found, Lexington Law advocates for their removal.

→ The final step, restore, focuses on ongoing support to address new credit issues as they arise.

Lexington Law offers various service levels catering to different credit needs, including bureau challenges/disputes, creditor interventions, inquiry assistance, ID theft insurance, and more. The company emphasizes leveraging legal standards to aid in the credit repair process.

So, they can help you navigate and understand – and even implement – complex issues like “Pay to Delete” and the intricacies of financial scoring.

Now, while Lexington Law has a track record of clients experiencing credit score improvements, as with all financial offers, individual results are going to vary (you can’t just expect that since something worked for some others, it will work for you too).

You might also like: How Does Self Credit Builder Work: The Big Picture

Who Can Take Advantage of Lexington Law’s Services?

I might have missed this if Lexington Law was available in my state, but not everyone is able to utilize Lexington Law’s credit repair offer – Lexington Law has no legal representation in Oregon, North Carolina, nor in outlying U.S. territories.

*So, Oregonians, North Carolinians, and non-mainland citizens will need to look elsewhere for credit repair solutions. If you’re in one of the other 49 states, keep reading…

If not, instead of enlisting a service, you could take a DIY approach – it may not be as hard as you think, if you’re committed to the credit repair journey.

You might also like: ASAP Credit Repair Review – Don’t Sign Up Until You Read This

How Much Does Credit Repair Cost With Lexington Law?

Lexington Law offers three service levels to cater to different credit repair needs that range from $99.95 to $139.95:

- Priced at $139.95/month plus taxes and fees, the Premiere Plus plan includes up to 8 challenges per cycle for Equifax and TransUnion, and up to 3 challenges for Experian. Clients receive up to 6 creditor interventions monthly, along with identity theft insurance covering up to $1,000,000.

- Priced at $119.95/month plus taxes and fees, Concord Premiere includes up to 6 challenges per cycle for Equifax and TransUnion, and up to 3 challenges for Experian. Clients receive up to 3 creditor interventions monthly, with identity theft insurance coverage up to $25,000.

- Priced at $99.95/month plus taxes and fees, Concord Standard includes up to 6 challenges per cycle for Equifax and TransUnion, and up to 3 challenges for Experian. Clients receive up to 3 creditor interventions monthly, along with identity theft insurance coverage up to $25,000.

Lexington Law’s billing operates similarly to a utility bill, with no upfront costs (you can sign up with $0 down). The first payment is due on day 5, covering initial work in monitoring credit and starting repair services. After that, billing takes place every 30 days.

You can cancel at any time, but it’s important to note that if you choose to do so, a final payment will be charged for work completed between the last payment and the cancellation date – And, late fees may apply if payments are declined due to insufficient funds or outdated information.

Lexington Law can be reached at (800) 341-8441 during business hours. If you find yourself unable to call them to cancel, check out your customer portal online or in the app. The specific process and timeframe for canceling or changing your Lexington Law program will be outlined in your membership agreement.

You might also like: Top 8 Best Credit Repair Books of All Time +Free Resources

Company Overview

Utah-based Lexington Law was founded in 1991 by John Heath. It’s a private, for profit, legal and financial consulting company headquartered in Salt Lake City.

Lexington Law is also the parent company for Credit.com.

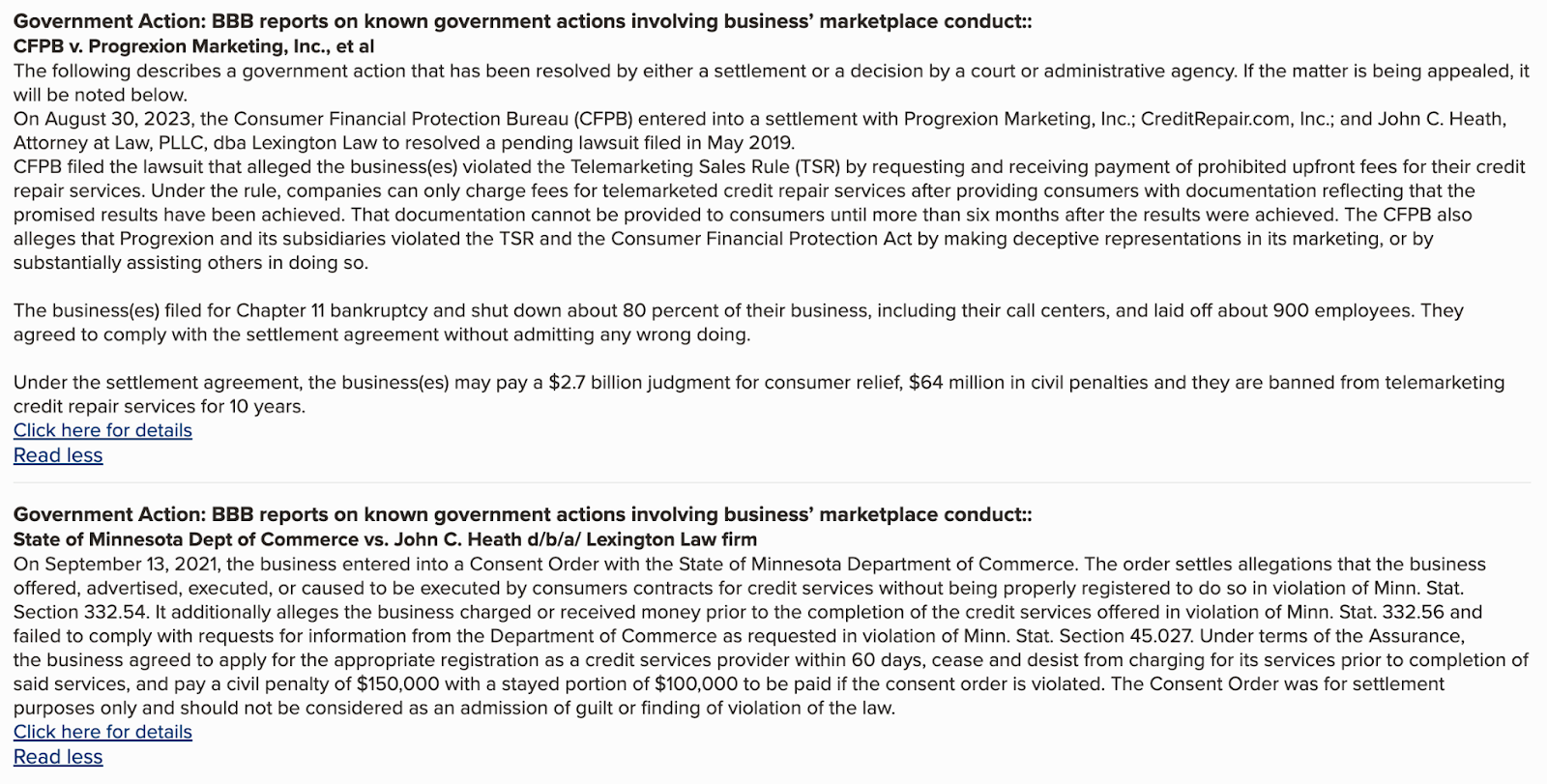

Unfortunately, the Better Business Bureau (BBB) has given Lexington Law an “F” rating – probably because they’ve been in the legal dog house a couple of times since 2019.

🚩 BBB lists info about a settlement involving Lexington Law. The government said they broke rules by charging upfront fees for credit help and making misleading ads. Lexington Law (and other companies) agreed to the settlement without saying they did anything wrong – They’re in financial trouble, having filed for bankruptcy, and they can’t do certain credit repair telemarketing for 10 years.

🚩Another issue involved the State of Minnesota, which shows they didn’t play by the rules for credit services. In this case, Lexington Law agreed to a settlement, paid a $150K penalty, and promised to follow the laws moving forward.

Despite the misadventures, they are still in business with legal credit repair reps working on behalf of consumers in 49 states.

Unfortunately, Trustpilot users can’t really vouch for them either. But, it’s more common for someone to review when they’re upset than when they’re content. And, Lexington’s still showing 4 and 5-star reviews from some of their clients.

While the fact that they’re still in business says something, Lexington Law seems to have seen better days. Nonetheless, let’s take a closer look at their service offering.

Lexington Law Service Features & Benefits

Lexington Law offers quite a bit more than just calling creditors and credit bureaus on your behalf – Their offer is pretty robust and (in my opinion) seems like it could be insanely beneficial. I think that if you were to take advantage of the offer with the promised outcomes, it would be well worth the monthly price tag.

So, what, exactly, can Lexington Law help you with?

1. Bureau Challenges/Disputes

First and foremost, Lexington Law takes on the task of challenging and disputing negative items on your credit reports. They work to question the accuracy and fairness of these items, aiming to improve your overall credit profile.

This service essentially involves contesting any inaccurate information on your credit reports. By doing so, it helps in rectifying errors and enhancing your creditworthiness. For example, if there’s an incorrect late payment record, challenging it could lead to its removal, positively impacting your credit score.

2. Creditor Interventions

Beyond challenging credit bureaus, Lexington Law engages with your creditors. This involves communicating with them to verify the accuracy and fairness of reported information, with the goal of resolving discrepancies and enhancing your credit standing.

Engaging with creditors is crucial for ensuring the information they report is correct. It’s a process of resolving disputes directly with the entities that provided the information. For instance, if there’s a discrepancy in a reported debt amount, intervening with the creditor could lead to a correction.

3. Inquiry Assist

Lexington Law assists in managing and addressing inquiries on your credit report. This service ensures that only legitimate and necessary inquiries remain, positively impacting your overall creditworthiness.

Managing inquiries is about overseeing who accesses your credit report. This service helps ensure that only relevant inquiries that align with your financial decisions are reflected. For example, if there are inquiries from unknown sources, addressing and removing them can prevent potential negative effects on your credit.

4. ID Theft Insurance

The service includes identity theft insurance, offering coverage in the event of identity theft. This protection provides financial assistance and support if your identity is compromised.

Identity theft insurance acts as a safety net in case your personal information is misused. It provides financial support to help recover from the consequences of identity theft. For instance, if your identity is stolen, the insurance would cover expenses related to legal help or lost wages during the recovery process.

5. DebtHandler

Lexington Law’s DebtHandler tool provides a personalized debt assessment based on your financial goals. It assists in creating a plan tailored to your objectives, whether it’s improving credit scores, reducing debt, or saving money.

DebtHandler is a tool designed to assess your debt situation and create a strategic plan. It aligns your debt repayment with your financial goals. For example, if your goal is to pay off high-interest debts first, DebtHandler can help structure a repayment plan to achieve that goal.

6. Report Watch Alerts

This feature provides real-time alerts regarding changes to your credit reports. It keeps you informed about positive, negative, and neutral developments, allowing you to proactively manage your credit.

Report Watch Alerts keep you in the loop about any changes to your credit reports. Staying informed helps you address credit-related matters promptly. For instance, if a new account is opened under your name without your knowledge, quick action can be taken to address potential identity theft.

7. TransUnion FICO Score

Lexington Law offers regular updates on your TransUnion FICO score. Monitoring your score allows you to track your credit progress and understand how your financial actions impact your creditworthiness. As a standalone offer, ongoing access to your FICO score usually costs $30+.

Regularly checking your TransUnion FICO score provides insights into your credit health. It’s a way to gauge the impact of your financial decisions on your creditworthiness. For example, if your score improves after paying down credit card debt, you can see the direct positive effect of that action.

8. Lost Wallet Protection

This service allows you to enter information from your wallet, purse, or mobile device. In case of loss or theft, Lexington Law may assist you in canceling or replacing your cards, contributing to the protection of your financial identity.

Losing your wallet is a financial horror story. Lost Wallet Protection is like having a superhero hotline, ready to save the day and keep your finances safe. For example, if your wallet is lost, quick action to cancel and replace cards can prevent unauthorized transactions and potential identity theft.

9. Junk Mail Reducer

This feature helps you opt out of pre-approved credit offers, places your phone number on a do-not-call list, and reduces the amount of marketing emails you receive. It minimizes unwanted solicitations, contributing to a more controlled and secure financial environment.

Junk Mail Reducer is a feature aimed at reducing unnecessary solicitations. It helps in creating a more focused and secure financial space by minimizing unwanted marketing communications. For example, reducing credit offers can prevent potential identity theft, and less marketing clutter can make

Frequently Asked Questions

Does Lexington Law fix your credit?

Lexington Law offers credit repair services by challenging inaccuracies on your credit reports. Their process involves disputing negative items with credit bureaus, aiming to improve your credit standing. Results vary based on individual circumstances.

Can Lexington Law help with late payments?

Yes, Lexington Law addresses late payments on credit reports. Through dispute processes with credit bureaus and engagement with creditors, they work to rectify inaccuracies related to late payments. It’s essential to note that outcomes depend on the specifics of each case.

Does Lexington Law call debt creditors for you?

Yes, Lexington Law may engage with creditors to verify and dispute information on your credit reports. While they actively work on your behalf, the extent of direct communication with creditors depends on the particulars of your case. They strive to ensure the accuracy and fairness of reported information.

How long does it take to see results from Lexington Law?

The timeline for results with Lexington Law varies. Some individuals may observe positive changes in a few months, while others may take longer. Credit repair is a gradual process, and the duration depends on factors like the complexity of your credit profile and the nature of the items being addressed.

How do I contact Lexington?

Contacting Lexington Law is straightforward. You can call them at (800) 341-8441 during business hours or reach out via chat on their website.

Final Thoughts: Is Lexington Law Legit for Credit Repair?

While Lexington Law doesn’t have the best recent track record, they have been helping consumers clean up their credit for over 40 years. Because of that, they’re pretty well regarded in the credit repair industry – Plus, the amount of satisfaction you can get from any service depends greatly on your expectations.

Personally, because of the recent lawsuits, I would pass on this one. However, this is a super robust offer with thousands of satisfied users. And, while some say the price tag is high, I will say that I’ve seen much higher.

Bottom line: you should be the one to decide if it’s right for you. Use what you’ve learned here to make that decision.

To get that credit score up fast so you can move forward with your life, check out Credit Secrets and start your journey to better financial health.

Ashley Kimler

Ashley Kimler is your friendly Credit Secrets wordsmith. With a knack for turning complex money matters into easy-to-digest advice, Ashley has been a trusted voice in the world of finance. With writing credits from Pangea Money Transfer, Centier Bank, Performio, and more, she's here to help you navigate the financial jungle with a dollop of wisdom. Let's turn sense into dollars together!