DIY Credit Repair Demystified (It’s Not as Hard as You Think)

So, you’re considering taking the DIY approach to credit repair? I’m a huge proponent, and I’m here to tell you that it’s not as difficult as you may think.

In 2014, my credit score was in the 300s – you can imagine what kind of derogatory marks I had with a score that low. What’s awesome is that I was able to boost it a couple hundred points within 60 days and buy a new car. A couple of years later, when I wanted to buy my first home, there was no problem (where even renting would have been a major feat before I repaired my credit).

Everyone’s credit profile is different, and you need a customized solution for the best results – this is why I’m a proponent of DIY credit repair vs credit repair services. But, it needs to be something you’re confident about spearheading if you want to be successful.

That’s where knowledge comes in…Congrats, you’re at the perfect starting point!

Here’s what’s in store:

- What is DIY Credit Repair?

- Is DIY Credit Repair Worth it?

- How to Repair Bad Credit on Your Own

- Tools to Help With DIY Credit Repair

- Frequently Asked Questions

- Final Thoughts

Now, let’s get goin!

What is DIY Credit Repair?

DIY credit repair, short for “do-it-yourself credit repair,” is like giving your credit score a little TLC on your own. Think of it as sprucing up your financial reputation.

Your credit score is like a report card for how you handle money. If it’s not looking great, DIY credit repair is your way to try and make it better without hiring a pro. It might involve checking your credit reports, disputing errors, paying your bills on time, and reducing debt.

It can also mean — in practical terms — that you avoid opening too many new accounts and that you stay patient. Anyone can do it, it just requires discipline and a little financial know-how. Plus, it’s a good precursor to keep your credit healthy in the long run.

You might also like: A Comprehensive Credit Versio Review: Is it Legit?

Benefits of DIY Credit Repair vs Credit Repair Services

Doing your own credit repair and using credit repair services both have their pros and cons. Here’s a quick breakdown.

The benefits of DIY credit repair:

- Cost-effective – DIY is usually free or low-cost, as you handle the process yourself without paying service fees.

- Empowering – You’re in control and learn valuable financial skills in the process.

- Private – Your personal information remains confidential because you’re not sharing it with a third party.

- Long-term habit-building – You can develop good financial habits that will benefit you beyond just repairing your credit.

The benefits of credit repair services:

- Hands-off – Professionals know the ins and outs of credit reporting, which can lead to more efficient and effective results.

- Time-saving – They handle the paperwork and negotiations, saving you time and stress.

- Credit industry relationships – Some repair services have relationships with creditors and credit bureaus, which could lead to faster resolution.

In a nutshell, DIY is cost-effective and educational, but it can be time-consuming and may not yield the same results as the most reputable professional services. Credit repair services offer expertise and time savings, but come with a cost.

The choice depends on your needs, budget, and how comfortable you are with managing your own credit repair efforts.

If you opt to work with a credit repair service, there are more risks involved, so you need to watch out for a few things:

- Never share your personal identifying information with someone who isn’t a licensed, reputable credit repair counselor.

- Beware of any credit repair professional who doesn’t make you aware of your rights under CROA.

Keep reading to learn more about how to take control over your own credit repair journey.

Is DIY Credit Repair Worth it?

I can read your mind, ‘Wow, Ashley, you’re making it sound like a lot of work. Will it be worth it in the end?’

Yeah!…It will. If your credit is already shot, spending money on a service and crossing your fingers in hopes that they deliver the results you’re after probably isn’t the best idea, right?

Well, if you opt for a DIY approach, you can take all the time you need.

And, your diligence will lead to better outcomes:

- Decreased bad debt

- Improved rates on loans and lines of credit

- The ability to finance a car or a home

- More favorable terms on future business credit opportunities

The amount of effort you put into DIY credit repair is up to you. And, the more you put in, the more you’ll get out of it.

Recommended: Applying for a Mortgage? How to Prepare Your Credit

How to Repair Bad Credit on Your Own

Before you read the following steps, I want to preface with the fact that credit repair can seem overwhelming, especially for beginners. But, these tactics aren’t as perplexing when you break everything down into bite-sized chunks.

I have a friend who often has to remind me, “when you’re cleaning your refrigerator, you only have to wipe one shelf at a time.” Sometimes, we make these types of projects seem bigger by zooming out when zooming in would be much easier.

Now, here’s how I would approach DIY credit repair…

Step 1: Learn Your Rights

When embarking on a credit repair journey, it’s essential to be aware of your rights as a consumer under the Fair Credit Reporting Act (FCRA).

Here are the basic rights you need to know:

- Right to access your credit reports – You have the right to obtain a free copy of your credit reports from each of the three major credit bureaus (Experian, Equifax, and TransUnion) once every 12 months through AnnualCreditReport.com.

- Right to dispute inaccurate information – If you find errors or inaccuracies on your credit reports, you have the right to dispute these items with the credit reporting agencies. They must investigate and correct any errors within 30 days, in most cases.

- Right to know who accessed your report – You can find out who has requested and viewed your credit report within the past two years. This helps you monitor for unauthorized inquiries.

- Right to add a statement of dispute – If you dispute information on your credit report and the credit bureau doesn’t remove it, you can add a 100-word statement explaining your side of the story.

- Right to fair and accurate reporting – Credit reporting agencies must ensure that the information on your credit report is accurate and fairly represents your credit history.

- Right to privacy – Your credit information is private, and it should not be disclosed to anyone without a legitimate business need to access it.

- Right to credit monitoring services – Some states offer free credit monitoring services to consumers if they’ve been victims of identity theft or experienced data breaches.

Understanding these rights is super important, because they empower you to take charge of your credit repair efforts and protect your financial reputation…And, if you believe your rights are violated, you can take action to rectify the situation.

Step 2: Obtain Copies of Your Credit Reports

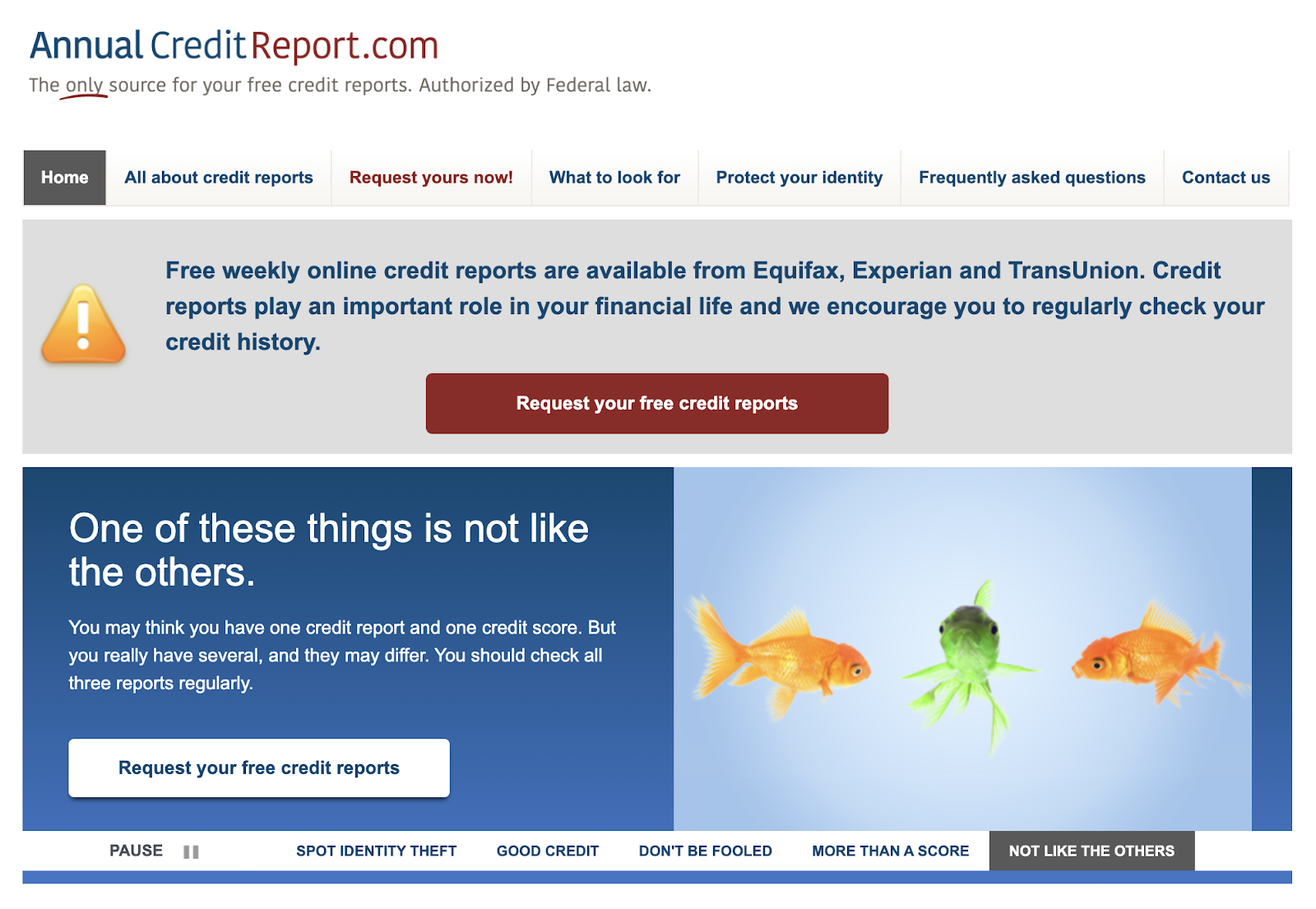

Getting your hands on those credit reports is a breeze. Here’s how you do it.

Go to your computer or phone and type “AnnualCreditReport.com” into your web browser. It’s the go-to spot for free credit reports. When the website loads, click “Request your free credit reports.”

They’ll ask for your name, birthdate, social security number, and a few other tidbits to confirm it’s really you.

You can choose reports from the three credit bigwigs:

You’re allowed one freebie from each every year. For a full financial picture, select all three.

Once you’ve picked ’em, you can download the reports or print them out. Easy peasy!

That’s it! You’ve got your credit reports in hand, ready to comb through them. Remember, you can do this once a year for free. So, keep tabs on your credit health and pull your reports at least once a year.

Step 3: Note & Dispute Inaccuracies On Your Reports

Now that you have your reports, you need to look for and dispute inaccuracies.

Let’s break it down in the simplest way:

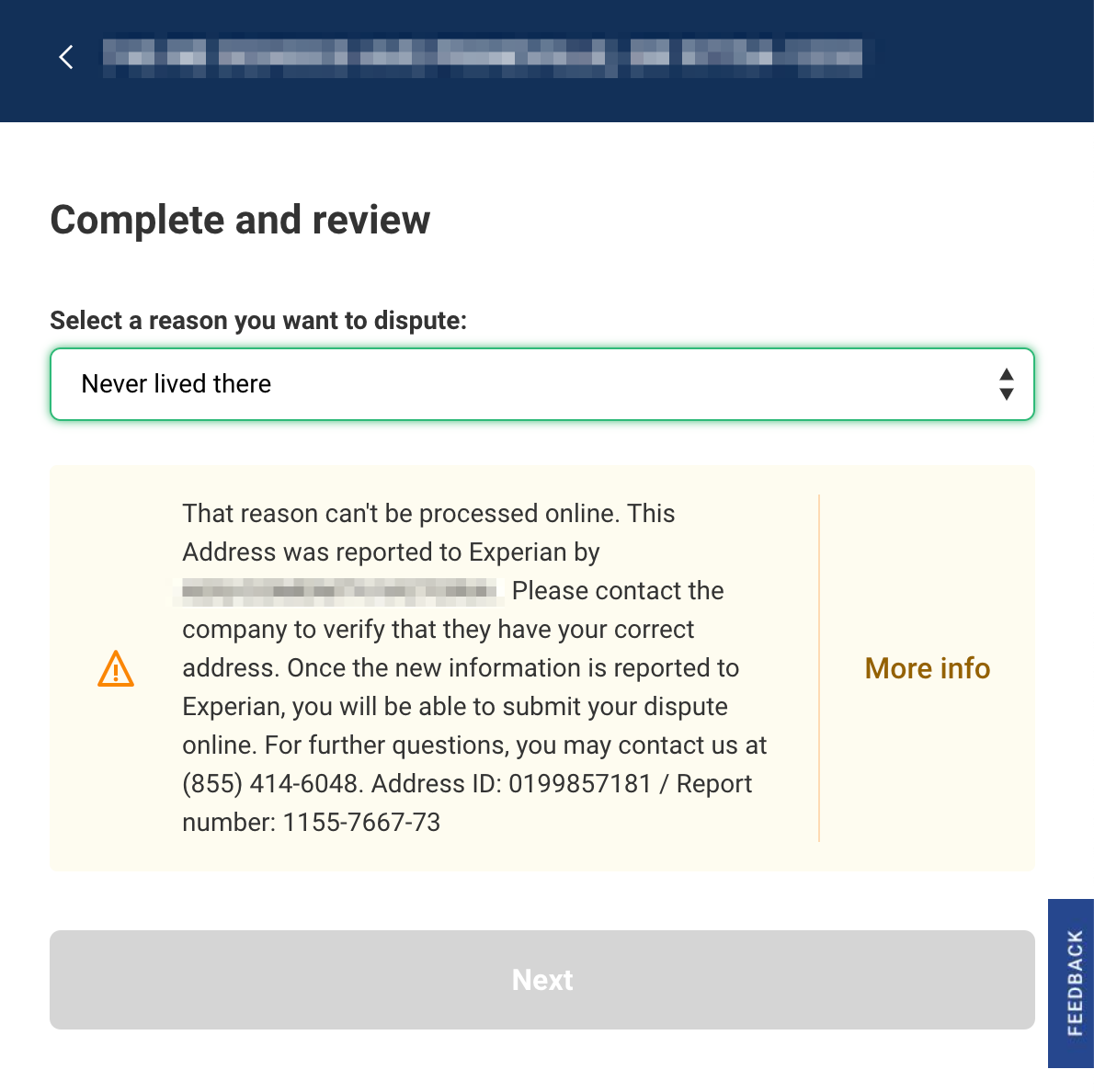

- Go through each of your reports with a fine-tooth comb. Look for any mistakes, like accounts you don’t recognize, payments that aren’t right, addresses you’ve never lived at, or inaccurate income.

- When you spot something fishy, jot it down. Make a list of the errors or discrepancies.

- Now, it’s time to tell the credit bureaus about these mistakes. Write a letter to each bureau (or use their online forms) to explain what’s wrong and why it’s a mistake. Be clear and provide any evidence you have.

- Mail your dispute letter or submit it online to each credit bureau that has the error. They have to investigate within 30 days.

- Be patient! The credit bureau will look into your dispute and let you know what they found. If they agree with you, they’ll fix the error.

Now, in some cases, you may not be able to dispute certain inaccuracies through the credit bureaus. For example, I just realized one of my creditors reported an incorrect address – In this case, it’s probably just a clerical error.

Regardless, Experian wants me to reach out to the creditor to make sure they have the correct contact information, then submit the dispute with the bureau.

That’s the basics! It’s like playing detective with your credit reports, and you’ve got the right to challenge any inaccuracies you find. Remember, staying on top of your credit is super important for your financial health.

Recommended: How to Improve Your Credit Score Fast: 5 Immediate Actions to Take

Step 4: Get Accurate Negative Marks Removed

There are several legal ways to get accurate, negative marks (excessive credit inquiries, etc.) removed from your credit report.

The most well-known way is to wait. After a couple of years, credit inquiries will fall off of your report. And after 7 years, missed payments will disappear too.

But, there are also proactive approaches you can take.

For example, you can “pay to delete” — Essentially, you would reach out to the creditor and ask for them to delete any negative remarks such as late payments in exchange for account payment in full.

Under the FCRA, I want to remind you that you have a right to do this; there’s nothing illegal about it…for now. FCRA doesn’t explicitly mention industry standards, and courts have often ruled against using them as legal grounds for claims.

However, in the future, the Bureau of Consumer Financial Protection (BCFP) could potentially change the rules. Plus, some say asking creditors to remove accurate items unfairly messes with the credit scoring system by erasing any record of charged-off accounts.

And, even if you pay off a collection account, it might still appear on your report, marked as “Paid,” in which case your scores won’t improve much.

That’s the gist of it! The “pay to delete” practice is a bit of a gray area in the credit world, and it’s unclear where things will go from here.

For more comprehensive secrets on how to legally improve more complex negative remarks from your credit report, check out Credit Secrets.

Step 5: Establish Optimal Payment History

Getting that A+ payment history on your credit report is like acing a class. Here’s how to do it.

First off, the golden rule is to pay your bills on time, every time — Seriously, this is the most crucial thing.

If you’re late with payments, it can really ding your credit score, like missing a homework assignment. So, mark those due dates on your calendar, set up reminders on your phone, or even use automatic payments if it helps. Just make sure those bills get paid on time.

Next, try to pay more than the minimum amount due on your credit cards. Think of it as going the extra mile in your assignments.

Paying just the minimum might keep you out of trouble, but it won’t boost your credit as fast. So, if you can, pay a bit more than the minimum to show that you’re responsible and serious about handling your debt.

Lastly, be consistent — Building a solid payment history takes time. Just like acing a class, it doesn’t happen overnight. So, stay on top of those payments and be patient. Over time, your credit report will shine with a stellar payment history, and you’ll be on your way to that top credit score.

Recommended: How to Build Credit History: The Fastest Way

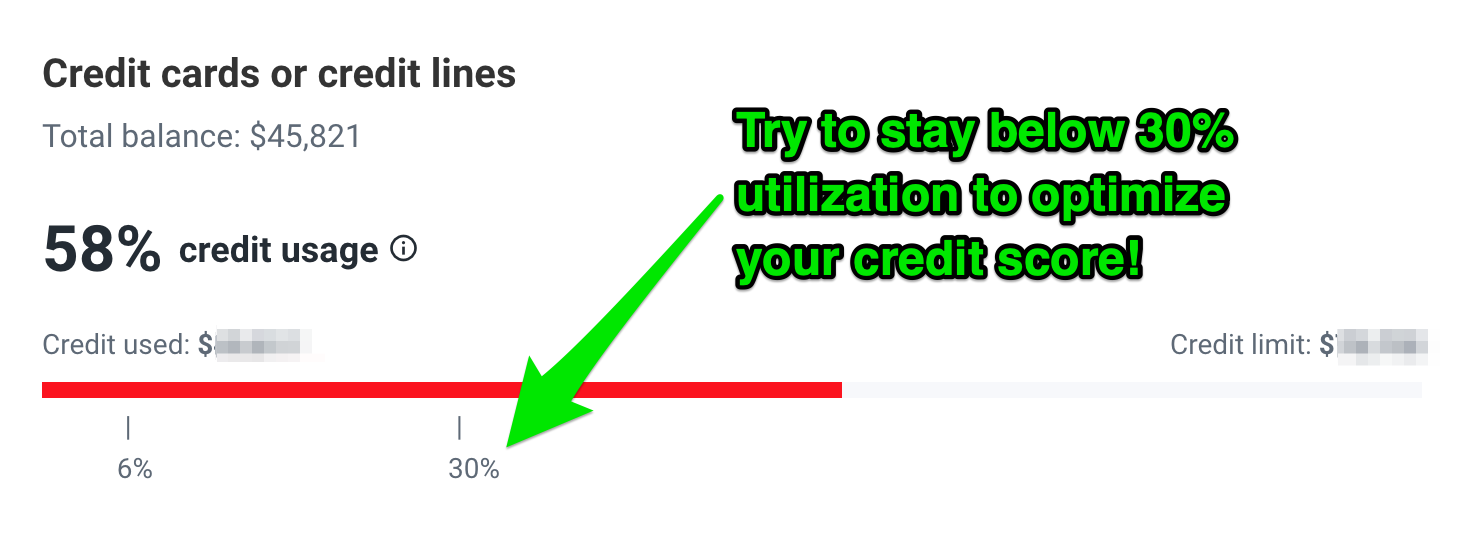

Step 6: Optimize Your Credit Utilization Ratio

In addition to making payments on-time, you need to be mindful of your credit card balances. Your credit usage, which is the percentage of your credit limit you’re using, plays a big role in your score.

Keeping this below 30% is like getting extra credit in class. It shows you’re not maxing out your cards, which is a good sign for credit bureaus.

If you’re above 30% utilization, you can either pay down your cards or – if that isn’t a viable option right now – you can apply for more lines of credit to increase your credit limit. But, be very careful with extending your credit.

If you’re already in the red zone, be sure you don’t just start overspending on new credit lines because it will only be harder to get out of the hole with more debt to repay.

To learn advanced techniques to get lines of credit with low or zero credit, check out Credit Secrets.

Tools to Help With DIY Credit Repair

Even if you’re tackling credit problems on your own, you don’t have to go in blind. There are tons of resources you can leverage to make your job easier. Let me share some tools that can provide tremendous value in your DIY credit repair venture.

Online Resources for DIY Credit Repair

DIY credit repair can be easier with the help of online resources.

Here are some handy options:

- Credit Karma — Credit Karma offers free access to your credit reports and scores. It also provides tips and tools for improving your credit.

- myFICO.com — myFICO, from the creators of the FICO score, offers educational resources and tools to help you understand and manage your credit.

- Credit counseling agencies — Nonprofit organizations like the National Foundation for Credit Counseling (NFCC) provide online resources and may offer counseling to help you manage your credit and create a plan for improvement.

- Government websites — The Federal Trade Commission (FTC) and the Consumer Financial Protection Bureau (CFPB) have resources on credit repair and credit reporting.

- Community forums — Websites like Reddit’s r/personalfinance and myFICO’s forums are places where people share DIY credit repair experiences and tips.

- Educational blogs & video channels — Many personal finance bloggers and vloggers offer free tips and tutorials on DIY credit repair. Just be sure to verify the credibility of the sources.

- Internet Archive – If you’re not already familiar, you might be pleased to discover archive.org, which is a free online library. It’s a treasure trove of information on all topics. Here, you can find tons of free books, movies, software, and audio about nearly any topic, including credit repair.

Remember, when using online resources, be cautious of scams and ensure you’re dealing with reputable sources. And, always double-check any advice or services you come across.

Recommended: ASAP Credit Repair Review – Don’t Sign Up Until You Read This!

DIY Credit Repair Books

DIY credit repair books are helpful resources for tackling credit issues on your own. These books typically offer step-by-step guidance and expert advice on improving your credit score. They cover topics like understanding credit reports, disputing inaccuracies, managing debt, and building positive credit habits.

Books can be a cost-effective way to access invaluable information and strategies to take control of your credit and financial future. It’s like having a credit expert in book form, guiding you through the process of repairing and maintaining good credit.

Recommended: Top 8 Best Credit Repair Books of All Time +Free Resources

DIY Credit Repair Letter Templates

DIY credit repair letter templates are pre-written, customizable letters you can use to communicate with credit bureaus, creditors, or debt collectors to address credit issues.

These templates make the process easier by providing a framework for disputing inaccuracies, requesting information, or negotiating payment arrangements. They save time and ensure your correspondence follows the necessary legal and regulatory guidelines.

In essence, these templates are like fill-in-the-blank solutions to help you communicate effectively and assert your rights in the credit repair process.

…Pssst…As a Credit Secrets member, you can access the Automator — which will streamline the dispute letter writing process — and more…

Frequently Asked Questions

What’s the fastest way to repair your credit?

Credit repair doesn’t have a quick fix, and it takes time. The fastest way is to focus on timely bill payments and reducing outstanding debt. As you consistently manage your finances responsibly, your credit score will gradually improve.

How can I fix my credit with no money?

You can start by reviewing your free annual credit reports for errors and disputing inaccuracies. Creating a budget to manage your finances and establishing good financial habits, like paying bills on time and reducing debt, can be effective and budget-friendly ways to improve your credit.

How do I remove a collection from my credit report?

To remove a collection from your credit report, you can negotiate with the collection agency for a “pay for delete” agreement. If they agree, ensure to get the agreement in writing before making any payment. Remember, there’s no guarantee this will work, but it’s a common approach.

Is credit repair high risk?

Credit repair itself is not high-risk, but you should be cautious of scams or unethical practices. Some companies may promise quick fixes or charge hefty fees upfront. DIY credit repair and working with reputable credit repair services are generally safe approaches, as long as you follow the proper procedures and avoid shady practices.

Final Thoughts

DIY credit repair may seem like a daunting task, but it’s entirely manageable. I’ve been there, with a credit score in the 300s, and I managed to boost it by hundreds of points in less than 60 days — The key is to be committed to the process and take it one step at a time.

So, what’s the takeaway? DIY credit repair is worth it. The time and effort you invest can lead to decreased bad debt, improved loan rates, and better financial opportunities in the future. It’s like taking a class where the more you put in, the more you get out. Your credit health is in your hands, and the knowledge you’ve gained is your best tool.

Now, it’s time to take the plunge and start your credit repair journey. Good luck, and here’s to a brighter financial future!

To dive deep into the world of credit repair fast and learn nearly everything there is to know about credit repair, check out Credit Secrets today.

Ashley Kimler

Ashley Kimler is your friendly Credit Secrets wordsmith. With a knack for turning complex money matters into easy-to-digest advice, Ashley has been a trusted voice in the world of finance. With writing credits from Pangea Money Transfer, Centier Bank, Performio, and more, she's here to help you navigate the financial jungle with a dollop of wisdom. Let's turn sense into dollars together!

What's Trending

{kind=link}