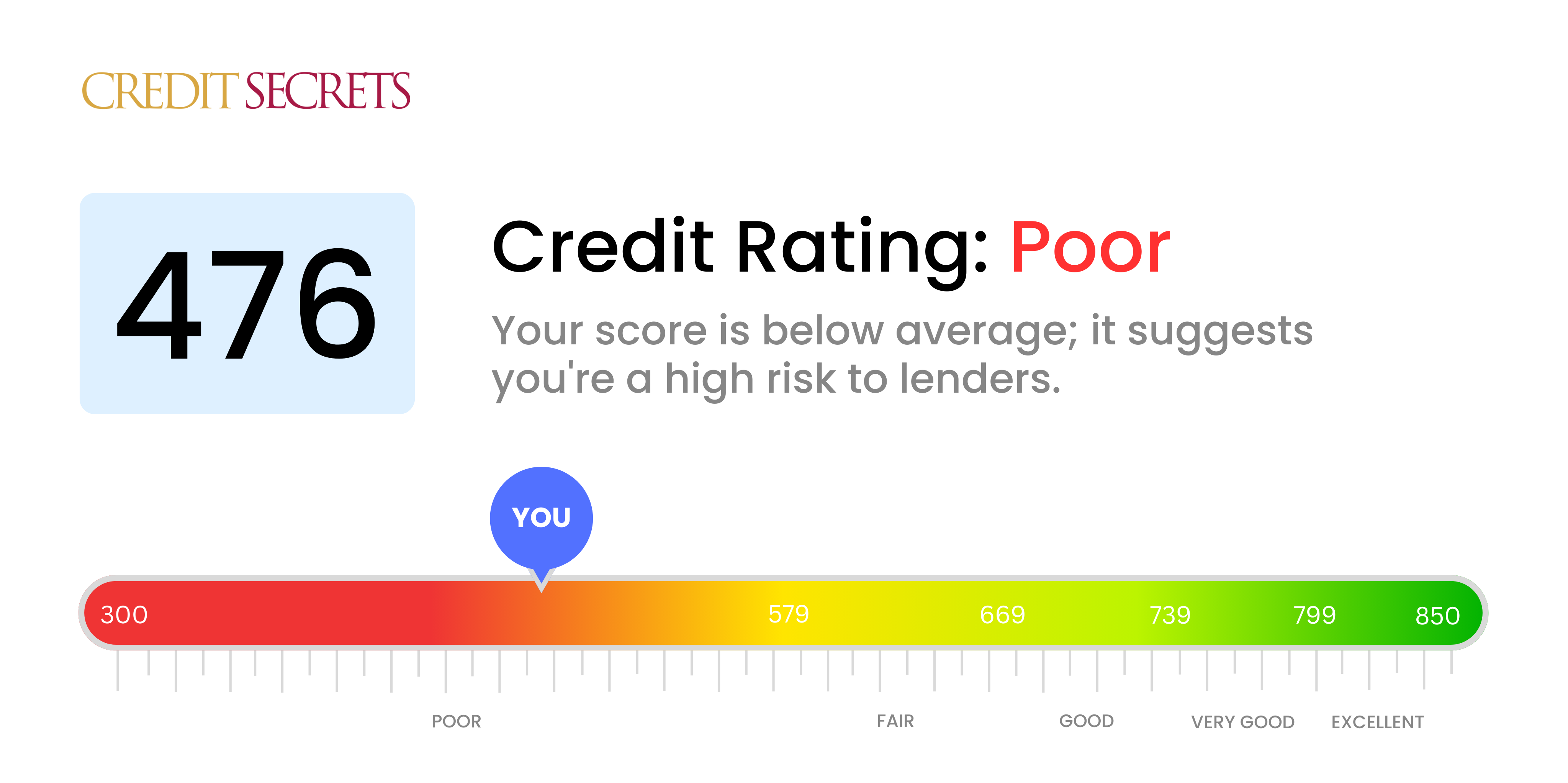

Is 476 a good credit score?

With a credit score of 476, it's clear that it falls into the 'Poor' category. This isn't the news you might want to hear, but don't lose hope - it's a situation that can be improved over time.

Given this score, you're likely to encounter difficulties when trying to obtain credit from mainstream lenders such as banks. This score suggests there may have been some past financial setbacks such as missed payments or defaults, hence it's considered risky by lenders. However, this isn't a permanent situation and with the right steps, you can rebuild your credit and aim for a better score.

Can I Get a Mortgage with a 476 Credit Score?

Regrettably, with a credit score of 476, securing a mortgage is likely to be a challenge. This score is significantly below the minimum that most lenders typically consider acceptable. A score within this range usually suggests a history of financial distress, such as late payments or failing to meet financial obligations entirely.

However, don't lose hope. While this may be a hard pill to swallow, it doesn't mean homeownership is out of reach forever. Alternative paths toward home ownership could be securing a cosigner with a better credit score or exploring government-backed loans that have more lenient credit requirements. Nevertheless, working towards improving your credit score should be a top priority. A higher score not only increases your chances of mortgage approval, but it can also provide you with better interest rates which can save you a substantial amount in the long run. Remember, the road to better credit is a marathon, not a sprint. It requires patience, diligence, and consistent financial responsibility.

Can I Get a Credit Card with a 476 Credit Score?

With a score of 476, it's unlikely that traditional credit card approval will come easily. This score often indicates to lenders a history of financial mishaps or challenges, making it a higher risk. Facing this reality can be tough, but it's essential for your financial path forward. Understanding your credit status is a vital first step to financial recovery.

However, there are alternatives to examine that could be better suited to your situation. Secured credit cards might be an ideal option; they require a deposit, that will set your credit limit. These cards could be easier for you to acquire and use to rebuild your credit gradually. You may also consider having a co-signer or focusing on pre-paid debit cards. These solutions won't solve all your issues instantly, but they could provide tangible help as you work towards restoring your financial health. Please note that the interest rates on credit options for low scores are often higher, reflecting the increased risk perceived by lenders.

Having a credit score of 476 may present some difficulties when trying to get approval for a personal loan. This score is significantly lower than what most traditional lenders consider within the acceptability range. Such a low score might make lenders wary, as it can represent a higher default risk. It's difficult to face these hurdles, but it's vital to understand what this credit score means for you when trying to borrow money.

There are alternatives you could explore. Secured loans and loans with a co-signer are two possibilities. In these cases, you provide collateral or another person with higher credit agrees to back your loan. Peer-to-peer lending might also be an option, as they sometimes have more flexible credit standards. But there's an important point to remember - these alternatives often have higher interest rates and stringent terms due to the increased risk to lenders. Despite the challenges, it's possible to navigate through the situation and find the right financial path for you.

Can I Get a Car Loan with a 476 Credit Score?

Navigating the road to securing a car loan with a credit score of 476 can be tough. It's important to understand that lenders often chase scores above 660 to determine if credit terms will be favourable. Sadly, your score of 476 falls well below the desired limit and is considered subprime. This might lead to elevated interest rates or even a denial of the car loan. The reason for this? A lower credit score is seen as a greater risk for lenders, indicating the potential for repayment difficulties in the past.

That said, a low credit score isn't a complete roadblock to a car loan. There are lenders who are willing to work with folks with lower scores. Be aware, though, these loans frequently have higher interest rates due to the perceived risk. Take the time to thoroughly research the terms and understand what you're signing on for. With tour diligence, a car loan can still be a achievable despite the challenges of having a low credit score.

What Factors Most Impact a 476 Credit Score?

With a credit score of 476, it's vital to determine the various factors that could have influenced this score to assist you in enhancing your financial standing. While each finance journey is unique, education and growth opportunities abound.

Repayment History

Late or missed payments could be a significant reason for your score. Such actions can harm your credit status.

How to Check: Examine your credit report thoroughly for any late or missed payments that could have damaged your score.

Credit Utilization

Having high credit utilization (approaching your credit limit frequently) can lower your score. If your card balances are near their capacity, this could be affecting your score.

How to Check: Scrutinize your credit card reports. Keeping the balances low relative to the limits is recommended.

Credit History Duration

The age of your credit can also impact your score. A shorter credit history may be detrimental.

How to Check: Evaluate your credit report to find the age of your oldest, newest, and the average age of your total accounts. Opening new accounts could unfavourably affect the score.

Credit Type Variety & New Credit Handling

An assortment of credit forms affect your score, and managing new credit carefully is crucial.

How to Check: Assess your credit accounts variety. Are you managing new credit judiciously?

Public Records

Public records, like bankruptcies or tax liens, could have a considerable influence on your score.

How to Check: Inspect your credit reports for any public records. Address any issues promptly to start improving your credit health.

How Do I Improve my 476 Credit Score?

Having a credit score of 476 puts you in the ‘poor’ category, but it’s not impossible to make adjustments and enhance that score. Here are a few tailored strategies for this scenario:

1. Focus on Delinquent Accounts

Accounts that have fallen into delinquency leave a substantial negative impact on your credit score. Prioritize bringing these accounts current by tackling the most overdue ones first. If you’re struggling, it’s perfectly fine to contact your creditors to possibly agree on a feasible payment plan.

2. Control Credit Card Debt

Credit balances that are high in relation to your credit limit can majorly influence your credit score. A suitable first step is to aim towards getting these balances below 30% of your limit, and gradually working towards keeping them under 10%. The highest utilized cards should be your initial focus.

3. Consider a Secured Credit Card

Given the condition of your current score, it might be tough to get a traditional credit card. A secured credit card can be a good alternative, as they demand a cash collateral deposit, which serves as your credit line. It’s important to use it wisely, only making small purchases and clearing the balance each month to establish good payment history.

4. Seek Authorized User Status

It might be beneficial to ask a close friend or relative with reliable credit if you could be an authorized user on their credit card. This could incorporate their good payment history into your credit report and can boost your score, as long as the card issuer reports authorized user activity to the credit bureaus.

5. Expand Your Credit Diversity

Having a varied combination of credit types can enhance your credit score. When you’ve established a good payment history with your secured card, consider new forms of credit, like a credit builder loan or retail card, and always handle these sustainably.