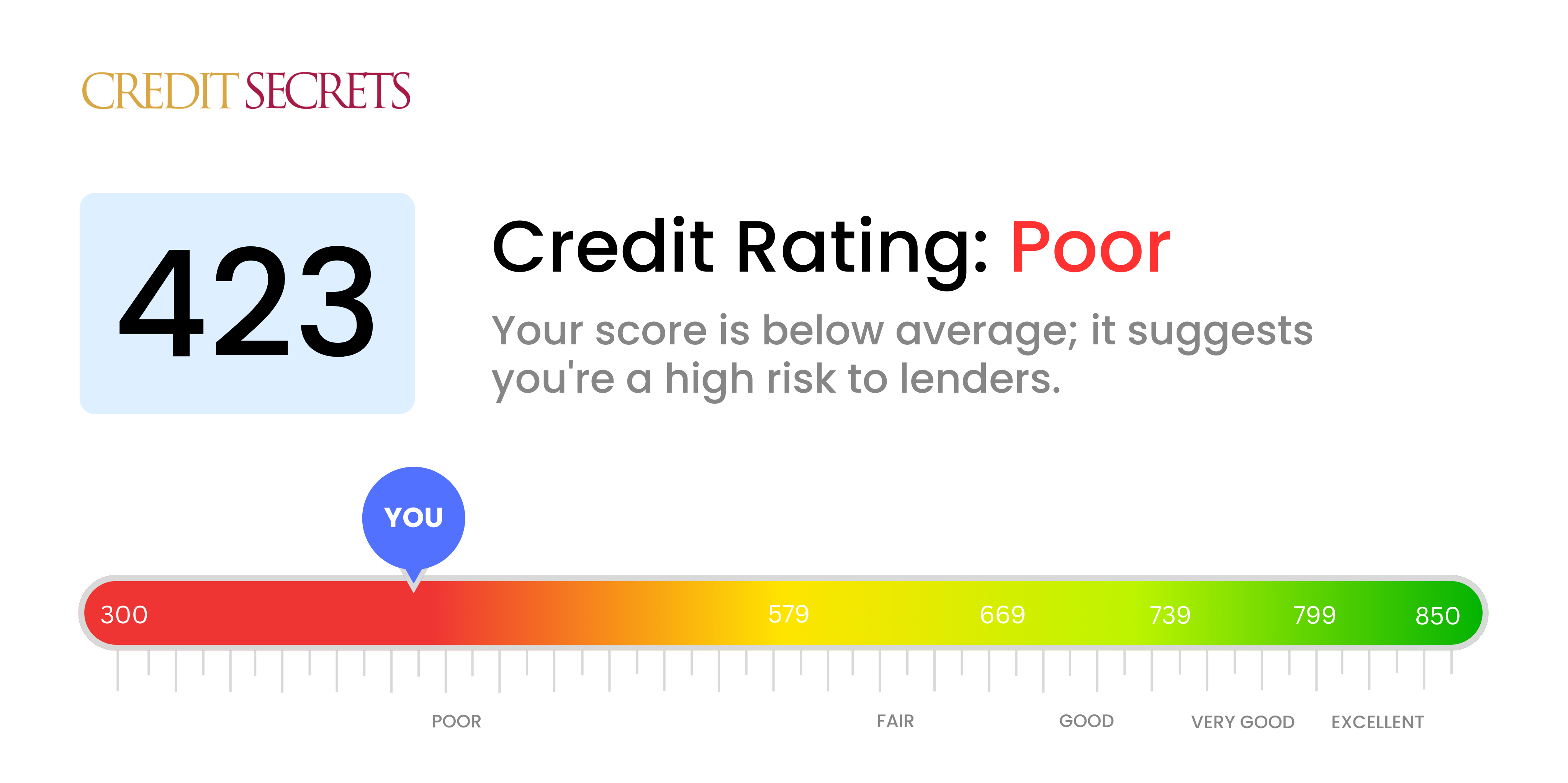

Is 423 a good credit score?

A credit score of 423 is considered poor by standard measures. Having this score often means it may be more difficult for you to qualify for credit cards, loans, and other types of credit tools, and if you do qualify, you might face higher interest rates. However, this doesn't mean you're out of options. There are various steps you can take to start improving your credit standing.

With proactive actions such as paying all your bills on time, reducing any existing debt, and avoiding new debt, you can gradually improve your score. Remember, this score isn't permanent and with time and responsible financial habits, it can be raised to a healthier range. Stay consistent with these habits and you'll likely see improvements, one step at a time. Just remember, slow and steady wins the race.

Can I Get a Mortgage with a 423 Credit Score?

With a credit score of 423, securing a mortgage approval is a significant challenge, mostly because this score suggests financial missteps in the past. Lenders prefer to see higher numbers since a higher score generally indicates a greater likelihood of regular payments. Your current score falls far below most mortgage providers' minimum requirements.

Although it might seem like a daunting problem, improving your credit score is indeed manageable. Begin by addressing any defaults or unsettled debts that could be hurting your rating. Once you've remedied those, establish a consistent pattern of timely payments to slowly build up your score. Improvement won't appear overnight, but with steady perseverance, a better score and stronger financial standing is highly achievable. Remember, lower credit scores often equate to higher interest rates, which means improving your score could also save you money in the long term.

Can I Get a Credit Card with a 423 Credit Score?

Having a 423 credit score can make obtaining a traditional credit card rather difficult. This score is viewed as high-risk by lenders, which indicates that there may have been financial difficulties or mismanagement in the past. It can feel disheartening, but acknowledging your current credit status is a key step in working towards financial rehabilitation. It's essential to face the reality, even if it might mean confronting some uncomfortable facts.

Because being approved for a regular credit card can be challenging with such a low score, consider alternatives like secured credit cards, which involve making a deposit that becomes your credit limit. These types of cards tend to be more accessible and can help rebuild your credit over time. It could also be worth thinking about having a co-signer or using a pre-paid debit card. While these options may not immediately solve the problem, they are helpful tools in moving towards financial stability. Keep in mind that any credit offered to consumers with lower scores usually comes with higher interest rates, as lenders see these situations as riskier.

With a credit score of 423, securing a traditional personal loan could be difficult. This score falls significantly below the range typically considered by most lenders and indicates a higher degree of risk in lending. It's tough to find oneself in such a situation, but it's an essential step towards improving your overall financial health.

Despite this, all is not lost. There are alternatives you might look into. Secured loans, where you provide an asset as collateral, or co-signed loans, where somebody else with a better credit score backs you up, are worth considering. You may also explore Peer-to-Peer (P2P) lending platforms as they can be more accommodating with credit score requirements. Remember though, these options can possess higher interest rates and less favorable terms due to the higher perceived risk. It's always crucial to carefully evaluate each path before any commitment.

Can I Get a Car Loan with a 423 Credit Score?

With a credit score of 423, your chances of securing approval for a car loan may be quite slim. Auto loan lenders typically seek scores above the 660 mark for favorable conditions, and anything below 600 is usually considered subprime. This means that your score of 423 categorizes you under this subprime bracket, which could lead to a higher rate of interest or even potential rejection of the loan application. It's simply because your lower credit score can signify a higher risk to lenders, as it suggests potential issues with paying back borrowed funds in the past.

However, don't lose hope. There are lenders who focus primarily on working with individuals who have lower credit scores. Keep a sharp eye and do some careful digging because these loans may come with significantly higher interest rates, as a result of the increased risk that the lenders have to take on. With careful planning and understanding of the terms, you still have the opportunity to secure a car loan. But also, remember not to make any hasty decisions and explore all of your options before making a final commitment.

What Factors Most Impact a 423 Credit Score?

Understanding your credit score of 423 is the first step on your journey toward better financial health. If you start by addressing the main contributing factors to this score, you're on the right course to improve it. Your financial journey is personalized and can be full of valuable lessons along the way.

Payment Consistency

Your credit score can be significantly impacted by your history of bill payments. Possible late payments or defaulting on debts are likely contributors to your current low score.

How to Verify: Check your credit report for any overdue payments or unpaid debts. Think about any instances where you may have paid late, as these could have affected your score negatively.

Credit Usage

If you're utilizing a high percentage of your maximum credit limit, this can adversely influence your score. If your credit card balances are maxed out, this could be one of the reasons for your low score.

How to Verify: Go through your credit card statements. Are your balances close to or at their limits? Striving to maintain balances low relative to your credit limit would be a beneficial practice.

Duration of Credit History

A short credit history can also negatively impact your score, particularly if new accounts have been added recently.

How to Verify: Analyze your credit report to evaluate the age of your earliest and latest accounts, and the average age of all your accounts. Take note if there have been recent additions of new accounts.

Variety of Credit

Possessing a diverse range of credit types and managing them well contributes to a good credit score.

How to Verify: Look at your mix of credit accounts, which could include credit cards, retail accounts, installment loans, and home loans. Reflect on whether you have been careful about applying for new credit.

Legal Judgments

Legal judgments such as bankruptcies or tax liens on your public records can significantly decrease your score.

How to Verify: Review your credit report for any public records. Address and resolve any issues mentioned.

How Do I Improve my 423 Credit Score?

A credit score of 423 indicates financial difficulties, but rest assured, there are recovery paths designed for these situations. This phase requires decisive, impactful steps to spark credit score recovery and financial progress:

1. Verify Your Credit Reports

Firstly, you need to review your credit reports from all the major credit bureaus. Ensure there are no errors or inaccuracies as these could unfairly impact your score. If you do spot errors, dispute them immediately.

2. Deal with Delinquent Accounts

An essential step is addressing any delinquent accounts. These accounts have a notable effect on your credit score. Communicate with your creditors, and if possible, set up a payment plan to start reducing the debt.

3. Apply for a Secured Credit Card

With your current score, obtaining a traditional credit card might be tricky. A secured credit card can be a solid alternative, given that it requires a refundable deposit. Use this card responsibly and aim to pay off the balance each month. Doing so will gradually improve your credit score.

4. Request Credit Limit Increase

Once you’ve successfully managed a secured card for some time, consider requesting a credit limit increase. This can lower your credit utilization ratio, assuming you don’t increase your spending, which potentially improves your credit score.

5. Consider Credit Builder Loans

After showing responsibility with a secured card, explore credit builder loans. These loans are designed to help build or boost your credit score. Make your payments consistently and on time as these payments are reported to credit bureaus, contributing positively to your score.