Business Credit vs Personal Credit: What Are the Differences?

If you’re an entrepreneur or small business owner, or if you want to be, you need to understand the differences between business credit and personal credit. While both types of credit are used to determine financial responsibility, each serves distinct purposes, and has a unique set of traits.

Here, I will give you everything you need to know about the differences between the two credit scores, bureaus, scoring systems, and financing options. We’ll look at credit in general, explore both business and personal credit in detail, then answer some of the most frequently asked questions.

This is what’s in store:

- An Overview of Business and Personal Credit

- How are Personal & Business Credit Scored?

- What Types of Financing Can You Get with Business Credit vs Personal Credit?

- Frequently Asked Questions

- Final Thoughts

Now, let’s get to it.

An Overview of Business and Personal Credit

First and foremost, credit is an indicator of financial responsibility. Both individuals and businesses have credit scores, which are numbers that indicate the entity’s “creditworthiness” – with all scoring systems that I know about, the higher the number or “credit score,” the better.

Credit scores are calculated by credit bureaus using various systems. Credit bureaus are institutions that collect and organize financial information about consumers and/or companies.

Credit makes it possible for individuals and businesses to obtain loans from major financial institutions in the form of credit cards, lines of credit, and traditional loans and mortgages with competitive interest rates.

Without credit, you may still be able to borrow money, but it will typically come with high interest rates, which means that it will usually cost more in the long run.

You might also like: Is 680 a Good Credit Score?

Who Can Obtain Business Credit vs Personal?

Let’s take a quick look at both types of credit in the U.S. and their key differences. Anyone can obtain credit, but proper registration as a business (business credit) or as a U.S. citizen (personal credit) is necessary.

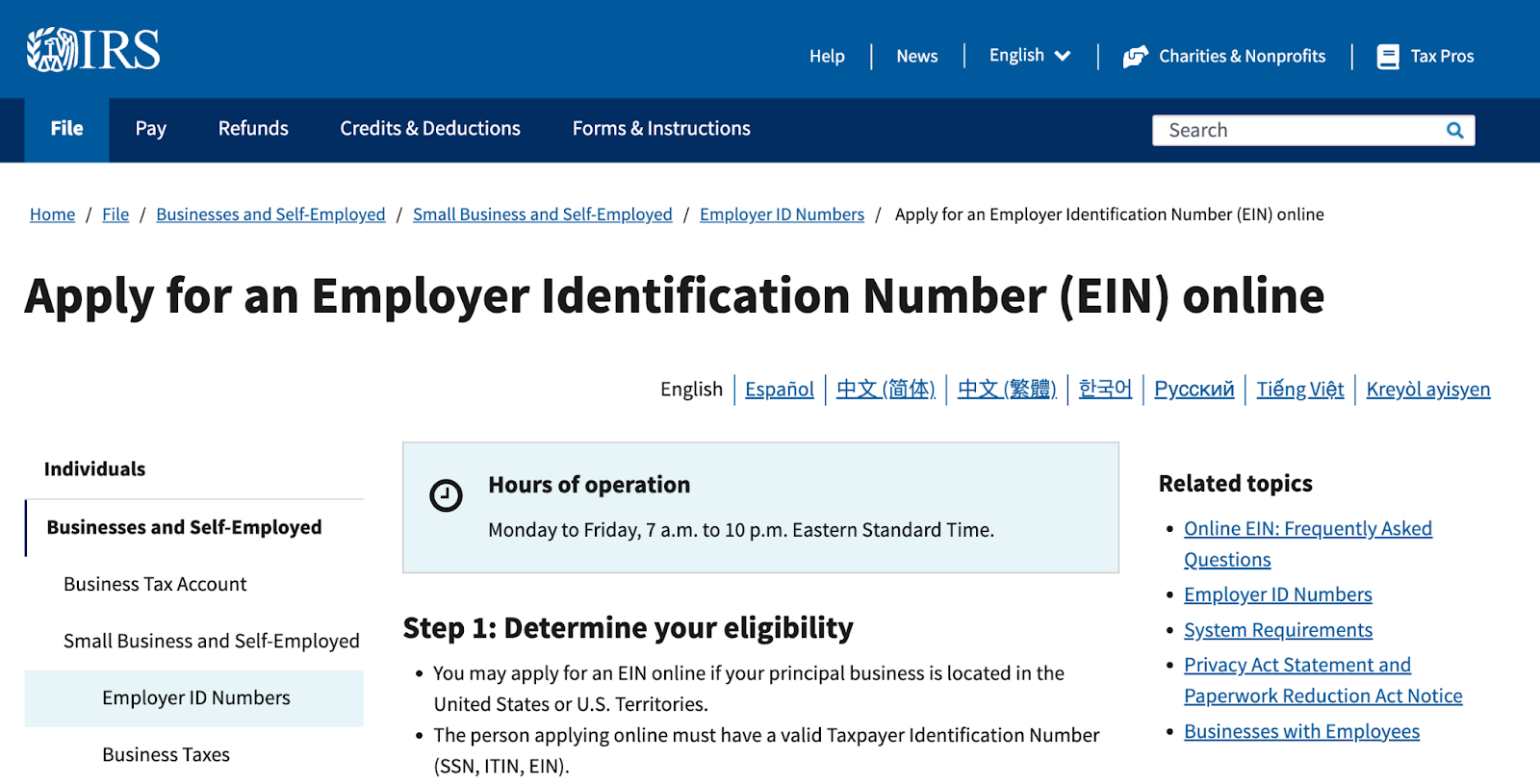

Business credit belongs to a registered business entity and is connected to an employer identification number (EIN) issued by the Internal Revenue Service (IRS). An EIN can be issued even if the business does not have employees.

If you need to register your business before applying for an EIN, you can do so through your Secretary of State website in your state of residence.

On the flip side, personal credit or “consumer credit” belongs to an individual and is connected to a social security number (SNN) issued through the Social Security Administration (SSA). Every U.S. citizen is issued a SSN and social security card at birth or within 14 days of applying after citizenship is established.

→ Request a SSN for the first time.

Both EINs and SSNs are free through their respective issuers, and the applications are simple. If you come across anyone trying to sell you an EIN or an SSN, they are providing an unnecessary service. Applying directly through the IRS and SSA respectively is the simplest way to obtain your identifying documents.

You can establish personal credit as soon as you have a SSN and you can establish business credit as soon as you have an EIN. However, businesses may require another identifying number, which I will explain soon.

You might also like: 15 Money Saving Tricks: Clever Ways to Grow Your Savings

Which Credit Bureaus Manage Credit for Personal Credit vs Business Credit?

The bureaus that manage personal credit are known as consumer credit bureaus – Those that oversee business credit are called business credit bureaus.

In the U.S., there are three major consumer credit bureaus:

- Transunion®

- Equifax®

- Experian®

While there are some outliers — the Consumer Financial Protection Bureau maintains a comprehensive list — most banks and major financial institutions rely on information from one of the above three bureaus when making credit decisions for individuals.

Now, where business credit is concerned, Transunion doesn’t get involved. Naturally, they do offer business services that help companies make informed decisions regarding consumer credit.

The three major business credit bureaus are:

- Equifax Business®

- Experian Business®

- Dun & Bradstreet® (D&B)

To establish credit with D&B you need your Data Universal Numbering System or DUNS® number in addition to an EIN. You may request yours once your business is properly registered, as they are automatically generated for most established business entities.

A DUNS® number through D&B is required for any business contract with a government agency, including employment contracts and federal or state grant applications.

You might also like: Here are the Top 15 Companies to Work for if you Want to be Happy

How are Personal & Business Credit Scored?

Credit is scored using various scoring models. Consumer credit scoring models are used universally by all consumer credit bureaus while each business credit bureau has its own scoring model.

There are two major consumer credit scoring systems in the U.S.:

- FICO Score

- VantageScore

Lenders, financial institutions, and individuals can access FICO Scores and VantageScores.

And, the three major business credit scoring systems are:

- Business Risk Score (Equifax)

- Intelliscore (Experian)

- PAYDEX Score (D&B)

Let’s take a quick look at how each of these scoring systems works.

You might also like: DIY Credit Repair Demystified (It’s Not as Hard as You Think)

FICO® Score

The FICO Score is a widely used credit scoring model that assesses an individual’s creditworthiness. It is based on credit history data from major credit bureaus and provides a numerical representation of credit risk.

These scores are important for people seeking various forms of credit, including mortgages, personal loans, and credit cards – Most major lenders use FICO Scores to evaluate the risk associated with lending money to a borrower. A FICO Score inquiry (when a lender pulls your credit) may have a small, negative, but temporary impact on your credit score.

FICO® Scores consider factors such as:

- Payment history

- Credit utilization

- Length of credit history

- Types of credit used

- New credit accounts

The score ranges from 300 to 850, with higher scores indicating lower credit risk.

VantageScore®

Similar to the FICO Score, VantageScore is another credit scoring model that evaluates consumer creditworthiness. It considers data from credit reports to generate a numerical score. VantageScore is the main consumer-facing credit scoring model.

VantageScore monitoring is beneficial for individuals seeking loans or credit cards. It may be used by lenders to assess the risk associated with extending credit to a borrower, usually during the pre-approval phase – a VantageScore inquiry shouldn’t impact your credit score.

VantageScore considers factors like:

- Payment history

- Credit age

- Credit mix

- Utilization

- Recent credit behavior

The score ranges from 300 to 850, with higher scores indicating lower credit risk.

You can access your VantageScore for free through credit monitoring sites like Experian Boost® and Credit Karma®. And, many banks and credit unions provide access to VantageScore as a courtesy to their account holders.

You might also like: This is How to Get the Most From Experian Boost Rent +More

Business Risk Score® by Equifax

The Business Risk Score by Equifax is a credit scoring model designed for businesses. It assesses the credit risk associated with a business entity.

Businesses seeking loans, credit lines, or partnerships can benefit from the Business Risk Score. Lenders and suppliers use it to evaluate the financial stability and creditworthiness of a business.

The Business Risk Score considers factors such as the business’s:

- Payment history

- Credit utilization

- Public records

- Financial stability

The score typically ranges from 101 to 992, with lower scores indicating higher credit risk.

→ See your company’s Business Risk Score®.

IntelliScore® by Experian

IntelliScore by Experian is a business credit scoring model that assesses the credit risk of a business entity based on various financial factors.

Businesses seeking loans, trade credit, or other financial arrangements can benefit from IntelliScore. Lenders and suppliers use it to evaluate the creditworthiness of a business.

IntelliScore considers factors such as:

- Payment history

- Credit utilization

- Public records

- Business size

The score typically ranges from 1 to 100, with lower scores indicating higher credit risk.

→ Access your business’ Intelliscore®.

PAYDEX® Score by D&B

The PAYDEX Score by D&B is a business credit scoring model that assesses how promptly a business pays its bills.

Businesses looking to establish credit relationships, secure loans, or engage in trade credit can benefit from the PAYDEX Score – as with the Business Risk Score and Intelliscore, many suppliers and lenders use it to gauge payment reliability.

It is a key factor in business credit assessments since the PAYDEX Score is based on a business’s payment history.

PAYDEX Scores range from 1 to 100, with higher scores indicating more timely payments. A score of 80 or above is considered favorable for creditworthiness (a score of 100 is perfect, but may be unbelievable, which can raise questions during underwriting).

→ View your company’s PAYDEX® Score.

What Types of Financing Can You Get with Business Credit vs Personal Credit?

In a nutshell, business financing offers are designed for common business expenses while personal financing offers cater to personal/consumer needs. In some cases, businesses can get higher limits than individuals, but this is dependent on income and credit scores.

Business financing comes in forms like:

- Business loans

- Business lines of credit

- Business credit cards

- Asset-based financing (ex: Real estate investor line of credit)

And, personal financing includes:

- Personal term loans

- Credit cards and lines of credit

- Mortgages

- Auto loans

- Student loans

I better add that there are many other types of financing that businesses and consumers can get. The above tend to be credit-score-based and come with the most competitive interest rates and most favorable repayment terms.

Do Banks Check Personal Credit for Business Credit?

In most cases, banks do check the owner applicant’s personal credit when they consider extending a loan or line of credit to the business. This is because most conventional business financing requires a personal guarantee – if the business defaults on repayment, the owner would be liable for the debt.

There are business funding options that require no personal guarantee (no PG) where the business owner is not liable to repay the money. But, these are usually corporate cards with pay-in-full terms or factoring-type funding. Neither funding type is usually credit-score-based.

No PG funding does not rely on the business owner’s credit score.

Corporate cards that offer credit are typically income-based. With corporate credit, you would get a line of credit based on business income and pay it in full each billing cycle, which is typically each month. Many modern corporate credit cards come with 0% interest, and some offer the chance to earn cash back and rewards.

Factoring type funding, which doesn’t often require a high personal credit score, comes in the form of:

- Accounts receivable or invoice factoring

- Merchant cash advances (MCAs)

- Working capital loans

- Equipment financing

- Factored term loans

- Other similar offers

In most cases, repayment terms for factored loans are based on a percentage of the business’ daily income. The downside is that factor rates are usually much higher than interest rates on conventional business funding. I think of factoring as the payday loan of the business world – in my opinion, you should only use it if you absolutely have to.

In sum, if you find a traditional business credit offer with no PG and a low interest rate, it’s a needle in a haystack.

You might also like: A Comprehensive Self-Help Credit Union Review

Frequently Asked Questions

How is business credit the same as personal credit?

Business credit both evaluate creditworthiness by looking at payment history, credit utilization, and credit history length. Whether you’re a business or a consumer, lenders use financial responsibility metrics to assess whether you’re a reliable candidate for credit extensions.

Does LLC business credit affect personal credit?

In the early stages, when your LLC is finding its footing, lenders usually request personal guarantees, which links you personally to the business debts. However, as your LLC establishes its credit history, the impact on your personal credit is reduced. Most of the time, you need a good personal credit score to get business credit, but you can eventually get much larger lines of credit once business credit is established.

Do you need a business credit card for an LLC?

While it’s definitely not required, a business credit card for your LLC has its perks – It provides a distinct credit identity for your business, simplifies expense tracking, and contributes to building business credit.

What are the disadvantages of a business using credit?

Credit for your business comes with both opportunities and risks. While it opens doors, there’s the potential for debt accumulation, growing interest charges (if you carry a balance), and an impact on cash flow (sometimes it’s positive, and sometimes not so much). Late payments can harm your business credit report, which influences your future borrowing capabilities.

What does your personal credit have to be to get a business loan?

Personal credit plays a backstage role in securing a business loan, especially for startups or smaller businesses. While there isn’t a specific magic number, a solid personal credit history very much enhances your chances of obtaining business credit because it signals to lenders that you are responsible and stable.

Final Thoughts

Overall, business credit and personal credit are designed for business and personal spending respectively. While there are many similarities with the way credit is scored and how lenders view financial responsibility, business and personal credit have several distinctions that set them apart.

Personal credit is managed by Transunion, Equifax, and Experian, while business credit aligns with Equifax Business, Experian Business, and D&B. And, scoring varies—personal credit uses FICO Scores and VantageScores, while business credit employs Business Risk Scores, IntelliScores, and PAYDEX Scores.

Banks often check personal credit for business decisions, usually they require personal guarantees. Recognizing these distinctions is crucial for navigating both personal and business credit landscapes efficiently.

To dive even deeper into the world of credit and get that credit score up fast so you can move forward with your life, check out Credit Secrets today!

Ashley Kimler

Ashley Kimler is your friendly Credit Secrets wordsmith. With a knack for turning complex money matters into easy-to-digest advice, Ashley has been a trusted voice in the world of finance. With writing credits from Pangea Money Transfer, Centier Bank, Performio, and more, she's here to help you navigate the financial jungle with a dollop of wisdom. Let's turn sense into dollars together!