How to Read and Understand Your Credit Report

Understanding a credit report can take a lot of work. It can be extremely confusing when you start to review it for accuracy. It’s as if numbers are scattered everywhere, and even wording can be confusing.

There are different sections, numbers, and parts that you should look out for.

Knowing how to read a credit report is not a fancy skill. It’s a necessity.

The road to being credit-worthy can be extremely bumpy if you don’t know how to read your credit report. You won’t understand how to use it to improve your credit score, get different types of loans, make purchases, or simply rent a house.

All these things can give you a headache. But once you understand it, reading credit reports becomes a piece of cake.

That’s what we hope will happen if you read this article till the end. In this blog, we’ll explain how you can read your credit reports, understand the major sections, identify errors, and much more. This will give you great insight into being financially literate and keeping your credit scores high.

Sounds fabulous, right?

So let’s get started.

What is a Credit Report, and Why is it Important?

A credit report is a comprehensive record of an individual’s credit history, providing detailed information about their financial behavior and credit-related activities. Compiled by credit bureaus:

- Equifax

- Experian

- TransUnion

These reports include data on all credit accounts, payment history, public records, and inquiries made by creditors. The primary purpose of a credit report is to offer a snapshot of the creditworthiness of a person. What does that mean?

Basically, it serves as a basis for assessing the risk associated with lending money or extending credit to the individual.

So here’s how it’s viewed.

Positive credit history = Responsible credit management

Lenders assess the level of risk associated with a borrower. Suppose you have a positive and lengthy credit history. Then, you’re more likely to receive loan approval. Why?

Because, based on your credit history, you’re what creditors consider “low risk.” Likewise, there are lower interest rates for people with good credit reports.

Lenders that see multiple late payments and charged-off accounts where you did not pay back the money lent to you will be less likely to extend any credit as they see you as “high risk.”

What Information Is On the Credit Report?

Now, let’s discuss the most important part of this article: what information is available on a credit report? Knowing this is helpful in understanding a credit report and how it works.

Personal Information

Personal information on the report gives a glimpse of who you are. This information includes:

- Name

- Address

- Date of birth

- Phone number

- Social security number

Any variations of your name spellings that you have used can also appear here, along with your current and previous employer’s. Typically, this can be your first and last name with a middle initial or even a maiden name.

The main thing you’re looking for in this section is that all your personal information is accurate and up to date.

Account History

This section shows account information that significantly impacts your credit report. It includes your credit card details, payment history, and current balance. This section also includes mortgages and loan information, i.e., student loans, installment loans, etc.

It is the longest section of your credit report. But how is this information gathered?

The creditors report this information to credit bureaus. It often includes more than two years of monthly balances in your account.

What is important about this section is understanding that all the information is being reported TO the credit bureaus BY your creditors.

Public Records

This section includes any bankruptcies you might have filed. These are recorded in the public records section.

This information reflects significant financial challenges and can be reported for over 7 years. Typically, a discharged Chapter 13 bankruptcy will only report for 7 years; however, a discharged Chapter 7 can report for 10 years.

Additionally, dismissed bankruptcies can be reported for 10 years as well. It is not uncommon for someone to file bankruptcy, not follow through to discharge, and still see the bankruptcy reported on their credit report.

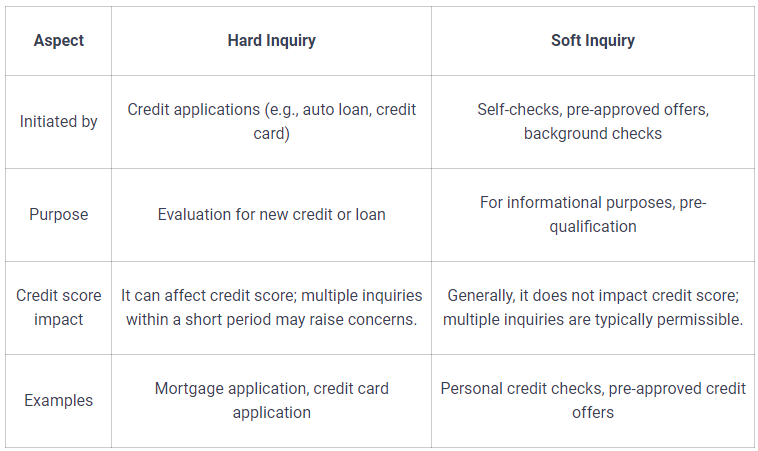

Credit Inquiries

There are two types of inquiries that you should know in your credit report. That’s why you should closely analyze this section. These inquiries include:

Hard Inquiries: These occur when a lender checks an individual’s credit report in response to a credit application.

Soft Inquiries: These inquiries are often from pre-approved offers or self-checks.

A hard inquiry typically occurs when you apply for any type of credit or lending, and the potential creditor accesses your credit report to assess your financial creditworthiness.

A soft inquiry can be current or potential creditors checking your credit report to monitor for changes or to see if you meet pre-qualification requirements for current credit offers. This type of check is a soft inquiry and does not impact your credit score. In fact, you’re the only one that sees these inquiries.

How to Read a Credit Report: A Step-by-Step Guide (for each section)

There is a lot of information on your credit report, and you need to be able to understand what that information is and how you can decode it. So here’s how to read each section of a credit report step by step.

Step 1: Understanding Personal Information

First and foremost, you should understand personal information. As mentioned earlier, it includes your name, address, etc. It’s extremely crucial for accurate credit reporting.

But why is it even necessary?

It’s essential because inaccurate personal information can make you susceptible to fraud. Additionally, creditors will use your current personal information and may reach out to you to verify and confirm that you are applying for credit with them.

If the wrong phone number is reported on your reports and the creditor cannot reach you, they may deny your application, or worse, they reach someone applying for credit in your name and approve the application.

Your personal information is one of the most important parts of your credit reports.

Step 2: Where Do I Find My Credit Score

When using a third-party credit monitoring service, you’ll usually find that your credit scores are displayed prominently at the very top. For example, a FICO score of 750 indicates a relatively healthy credit score standing.

If you want your credit scores directly from the credit bureaus and not through a credit monitoring service, then you can purchase them directly from the bureaus.

There are different credit score ranges. You should check these and do a comprehensive review of where you stand. It also gives you a glimpse of what a credit report looks like.

But what if you can’t find your credit score anywhere?

It’s available in 3rd party credit monitoring reports, and here are some other ways to find it:

- Check with the credit bureau

- Use online tools and websites

Step 3: Deciphering Account Information

This credit report information is the most crucial aspect of informed financial planning. You should review whether accounts are open, closed, or in collections. There are two aspects to this. If you see a credit card marked as

- Closed by consumers indicates a deliberate action. Typically not considered negative.

- Closed by the grantor indicates a non deliberate action. Typically not considered negative.

- Charge-off suggests unpaid debts. Typically considered negative.

Closely look at all the aspects and assess balances on your credit report. Examine payment histories to check credit management and what areas you need to improve. A history of late payments will have a negative impact on credit scores.

Step 4: Interpreting Public Records

Bankruptcies are part of the public records section of your credit report.

If you have a bankruptcy, getting loan approvals and renting a home can be challenging. Here’s how it works:

Bankruptcy reporting → Low credit score → Poor credit report → Fewer opportunities → High interest rates → Reduced loan approvals.

Step 5: Making Sense of Credit Inquiries

There are two different types of inquiries. This credit report information is vital to understanding what impacts your financial history. Here’s a table of the difference between a hard and soft inquiry.

What Information Is Not On a Credit Report

Here is a list of personal information that is not found on your credit reports:

- Salary

- Employment status

- Marital status

- Spouses credit history

- Assets

- 401(k) loans

Common Credit Report Mistakes and How to Dispute Them

Imagine you’re taking an important exam. The questions were quite difficult, yet you managed to answer everything perfectly. But you made one mistake.

You wrote the wrong name and registration number. That’s a terrible mistake. Right?

Likewise, on your credit report, even small mistakes can have a huge impact on your credit report. Here are some of the most common mistakes and how to resolve them. Now that you know what information is on a credit report, let’s dive deeper into credit report information errors.

Incorrect Personal Information

Check for your details, such as name, phone number, address etc. Check each credit bureau to ensure that all personal information is reported accurately. Suppose your personal information is wrong. How can you resolve it?

Here’s how.

After spotting credit inaccuracies, contact the credit bureau. Include supporting documents, such as a copy of your government-issued I.D. and utility bills, for identification purposes. This plays a significant role in verifying the correct information and quick dispute process.

Regularly check your credit report to ensure corrections are made.

Inaccurate Account Information

Inaccurate account information on your credit reports can include errors in payment history, account status, account balances, etc. For example, your credit card balance is $500, but the report says $1,000; this significantly impacts your overall utilization, impacting your credit score. You must scrutinize and note the discrepancies.

Reach out to the creditor associated with the inaccuracy. Discuss the issue and rectify it. But what if the creditor doesn’t solve the problem? What step should you take next?

You should file a dispute with the credit bureau. This helps update the credit report with the right information.

Unfamiliar Accounts or Inquiries

If you discover accounts reporting on your credit reports that you have never had and have no knowledge of, you have the right to create an FTC Identity Theft Report.

The FTC Identity Theft Report helps you prove to the creditor that someone stole your identity, and having this report makes it easier to correct problems caused by identity theft. Please visit www.identitytheft.gov to file your report.

After you file your report you can use the letter found at https://www.identitytheft.gov/Sample-Letters/identity-theft-credit-bureau and send to whichever bureaus are reporting the account on your credit file.

You should also review your credit inquiries to be sure there is nothing that you’re unfamiliar with.

Your Rights Under the Fair Credit Reporting Act (FCRA)

The Fair Credit Reporting Act (FCRA) is a federal law designed to protect consumers’ rights. It ensures the accuracy, fairness, and privacy of information in your credit report.

Your credit report information is crucial, and understanding your rights is essential. Because it helps maintain full control over your credit information.

Rights Consumers Have Under the FCRA

Being aware of your rights helps you make the right decisions for yourself. Here are some of the rights consumers have under the FCRA.

- Access to free annual credit reports.

- Notification of adverse actions with specific reasons.

- Right to dispute inaccuracies in credit reports.

- Opt-out option for prescreened credit offers.

How the FCRA Protects Consumers

The FCRA mandates accurate and up-to-date information on credit reports. Not everyone has access to the credit reports. But how’s that beneficial for you?

It means you have privacy and your data is secure. The credit reporting agencies have to maintain a certain level of security. Thus minimizing the risk of data breaches and victims of identity theft.

But who’s allowed to get access to your personal credit report?

- Creditors for credit applications.

- Employers with your consent.

- Landlords for rental assessments.

- Insurance companies for premium determinations.

How to File a Dispute Under FCRA

To file a dispute under the FCRA, you need to know what information is on your credit report.

This way, you can point out any inaccuracies or errors and write a letter to the credit bureau detailing the inaccuracies.

Attach relevant documents, such as monthly payment receipts or correspondence with creditors, to substantiate your dispute. Don’t attach original documents. Instead, add a copy of these. It will strengthen your case and increase the chances of the bureau making changes.

What should you do next?

Regularly check your credit report. Ensure corrections are made. Follow up with the credit bureau to confirm the resolution.

How to Read and Analyze Your Credit Report with Expert Guidance from Credit Secrets

Your credit report is a powerful financial tool that can transform your financial situation. Regularly review your credit report to help maintain good credit. By following the tips in this guide, you can understand a credit report and learn how to read it.

Your credit report is like your report card that determines your financial health. It is important for your financial life and for renting or buying a home, taking out loans, and many other aspects of life. It’s best to be financially aware. Take the first step towards securing your finances by getting expert advice from top credit resources committed to helping you gain the knowledge you need to improve your financial health.

Jenn Cartwright

Jenn is the lead credit coach and head of customer success at Credit Secrets.

She transformed her own credit story from a modest beginning into an inspiring tale of financial triumph using the Credit Secrets program.

Originally a customer back in April 2017, she not only soared her scores from the low 400s to the 700s within 6 months using the Credit Secrets program, but also delved deep into the credit cosmos, exploring courses, consumer laws, and even co-hosting webinars with the nation's leading credit expert, John Ulzheimer.

Now, she funnels her passion and expertise into ensuring everyone has access to clear, concise, and actionable information to improve their credit scores and unlocking their financial freedom.