A Complete Guide to Bankruptcy Recovery and Credit Rebuilding

Bankruptcy is an overwhelming experience, but it also acts as a stepping stone towards a brighter financial future. It allows you to make a fresh start on your finances.

There are many challenges that come along the way. One of the primary things is that credit scores start declining rapidly. Additionally, once the bankruptcy is reported to your credit reports, it can be legally reported for ten years.

However, if you take the right steps, the negative effects can fade with time. So, what are the right steps? How to recover from bankruptcy?

This guide will comprehensively answer the most common questions we receive, as well as discuss life after bankruptcy and much more. Not only this, we’ll also discuss how you can successfully work on rebuilding your credit after bankruptcy.

So keep reading.

Understanding Bankruptcy and Its Impacts

Before making a recovery plan, you should check your credit reports, review their accuracy, and immediately dispute any incorrect entries. The dispute process will differ depending on the type of bankruptcy you file.

CHAPTER 7 Bankruptcy

If you file Chapter 7 bankruptcy, you should wait until your case is discharged. The court will inform you by issuing a “Discharge of Debtor” when the case is finally done.

Your credit report should be updated with all the bankruptcy information within that period.

You can request your credit report from all three major credit bureaus. But how will you know that accounts are under bankruptcy?

The creditors are required to report that the account has a zero balance and was “included in bankruptcy.”

These accounts can also labeled as “discharged in bankruptcy” or “discharged”.

Here’s one thing that you must look for: if there are debts, such as mortgages, etc., that are excluded from the bankruptcy filing, ensure they are not listed as discharged.

CHAPTER 13 Bankruptcy

In the case of Chapter 13 bankruptcy, your case won’t be discharged until the end of your three-to-five-year repayment period. The status of your different accounts may or may not be impacted.

Moreover, in this, creditors are not obliged to report payments. Once your repayment period ends, your case will be discharged. However, your repayment plan also plays a significant role in it.

Even though creditors frown on seeing bankruptcy, they frown a little less when they see it was a Chapter 13 because it signals that you did your best to repay what you borrowed.

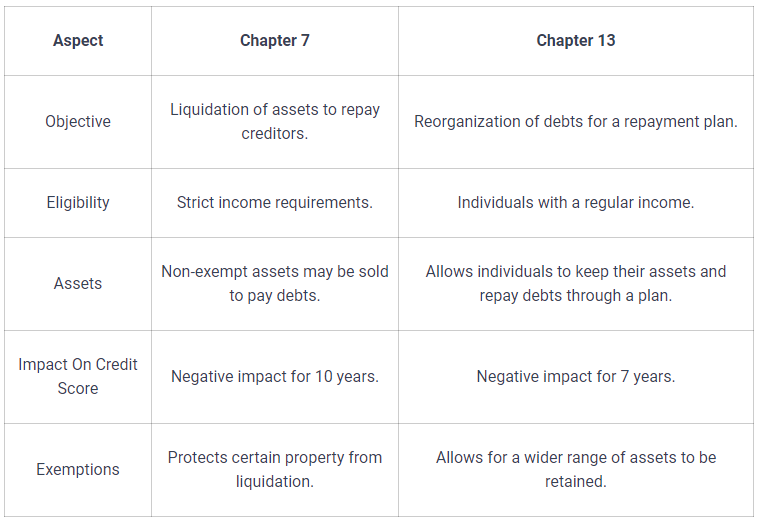

Here’s a summarized view of the major differences between Chapter 7 and Chapter 13 in a table form. It also highlights how long a bankruptcy affects your credit.

Now that you know how bankruptcy affects your credit, you should also know its drawbacks. Bankruptcy can have a huge impact on your credit score as well. It ultimately lowers your credit score, which means a lot of new financial hurdles.

- Higher interest rates

- Difficulty in renting a house

- Unable to get loans from banks.

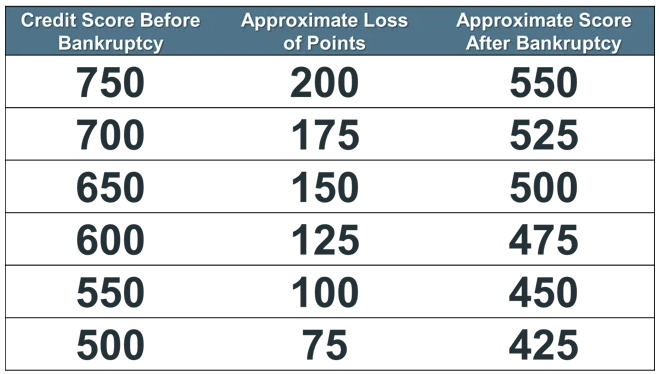

Here’s how filing for bankruptcy can impact your credit scores.

Filing for bankruptcy can also lead to mental distress, depression, etc. However, seeking emotional and mental support during this period is important, whether through friends, family, or professional counseling. It’s essential to have a support system in these difficult times.

The Road to Recovery: Life After Bankruptcy

If someone has faced bankruptcy, what should they do? What should be their immediate next step?

Most people take action too late, which causes the problem to worsen. However, that shows us why it’s crucial to be financially literate. Here are quick steps to take after bankruptcy is finalized.

- Review and understand post-bankruptcy documents, including the discharge order.

- Notify relevant parties (creditors, landlords) promptly about the bankruptcy discharge.

- Confirm closure of the bankruptcy case with the court for legal acknowledgment.

- Obtain and review updated credit reports to monitor credit status and identify any errors.

- Look for a credit product such as a secured loan or secured credit card.

- Establish a realistic budget, allocating funds for necessities and potential debt repayment.

Bankruptcy carries a huge emotional weight. It’s important to shift your mindset. Don’t view it as a failure.

Instead, look at it as an opportunity to do better than last time.

Individuals suffering from it should be encouraged to go without guilt or stigma associated with financial challenges.

However, all the motivation is useless if you don’t cultivate new and healthy financial habits. They push you to success and set the stage for long-term stability and success. These credit habits improve your financial situation a lot.

Creating a Post-Bankruptcy Budget

Life after bankruptcy can be tough. But with proper planning, you can reduce the stress that comes with it.Taking steps such as creating a post-bankruptcy budget, and getting a secure credit card are two great first steps.

So what is a post-bankruptcy budget?

A post-bankruptcy budget is a financial plan developed after successfully exploring bankruptcy proceedings. Every person should have this. But many people make mistakes while making it, so here are some fundamentals you must know.

Make a list of your revenue streams, such as jobs, side hustles, etc. Distinguish between:

- Necessary expenses (e.g., housing, utilities, groceries)

- Non-essential expenses (e.g., entertainment, dining out).

Allocate a portion for savings to ensure a financial cushion and support future goals. Track your finances regularly.

But is keeping track of your finances necessary?

Yes, for bankruptcy recovery, this is extremely crucial. You can identify your spending patterns and make adjustments based on that. So, your budget remains a helpful tool that adapts to evolving financial circumstances.

You should always have a financial safety net. This budget will act as that.

So, how long does it take to recover from bankruptcy?

It depends on every individual situation. You should have enough savings to buffer against unforeseen expenses so you never fall into financial distress again.

Rebuilding Your Credit Step by Step

Get a secure credit card

If you want to work on rebuilding credit after bankruptcy, you must know about secured credit cards. These cards require a security deposit, acting as collateral, and typically have lower credit limits.

But how can you use it for building credit after bankruptcy?

By responsibly using and making on-time payments on a secured credit card. This way, you can showcase your creditworthiness over time. Pay your bills on time to build a strong financial profile. A positive payment history will accumulate through this, and that’s how to rebuild credit after bankruptcy.

Get a secured loan

There’s another significant thing that you should know: credit builder loans.

These are designed specifically to help individuals establish or rebuild credit. Here’s how it works.

Borrowed funds are in a locked account → Borrower keeps making monthly payments → The term is concluded → Borrower gets access to funds and usually the interest paid toward the loan too.

Keep making payments on time

If you pay on time, then this will also leave a positive impact on your credit history. Do you know the foundation of a positive credit history?

It is timely payments.

They showcase that you’re financially responsible. Avoid late payments. A quick fix to this problem is setting up automatic payments. That way, you don’t have to worry about on-time payments.

*Tip* Be sure to log in to your accounts each month and confirm that the auto-pay feature is working properly and making your payments.

If you want to improve your credit profile, being financially educated is very important. It’s no secret that Credit Secrets is a solid financial and credit improvement guide. This comprehensive book includes insights, tips, and strategies for understanding the complexities of credit repair and enhancement.

Additionally, if you’re looking for lenders to see you as a “Better Borrower,” we have amazing credit builders. The Secret Credit Builders are installment & revolving lines of credit that can add positive accounts to your credit profile. The best part is that there are no hard inquiries.

Monitoring Your Credit Post-Bankruptcy

It would be best if you did not make any mistakes after bankruptcy. One mistake can make the rebuilding and recovery process even harder. So what should you do?

You should know your credit standing. That’s only possible if you know how to review your credit report. There are three major bureaus:

- Equifax

- Experian

- TransUnion.

Inaccuracies on your credit report can make life after bankruptcy even more challenging. Why?

Because it can lead to major problems such as identity theft, account usage, improper payment issues, and much more, here’s a quick step-by-step process for disputing errors on credit reports.

- Request free reports from Equifax, Experian, and TransUnion. Examine each section for errors impacting your credit.

- List inaccuracies with account names, dates, and relevant details.

- Collect evidence (receipts, correspondence) supporting your dispute. State errors, explain inaccuracies, and attach supporting documents like credit card statements.

- Mail the dispute letter and documents via certified mail with the return receipt. Allow the credit bureau 30 days to investigate.

- Check the results sent by the credit bureau after the investigation. If issues persist, dispute directly with the creditor using the same documentation.

- Regularly check your credit report to ensure corrections are maintained.

Many people prefer using credit monitoring services. Why?

Because they provide ongoing surveillance of your credit report, they offer continuous tracking of credit reports, timely alerts for any changes or suspicious activities, and additional tools to aid credit recovery. But how do they make it possible?

By understanding the factors influencing your credit score. After identifying it, you can tailor your financial behavior to optimize credit recovery. In short, they tell you what to do after bankruptcy.

Not only this, they have up-to-date information. You can make more informed financial decisions. It includes managing existing debts, exploring credit opportunities, and avoiding actions that may negatively impact your credit.

Common Pitfalls to Avoid in Bankruptcy Recovery

Many people make mistakes when finding the way toward bankruptcy recovery. That’s why we’ll tell you some common mistakes people make that have severe negative impacts. So you don’t do that at all.

Taking on too much credit too soon

Resist the temptation to rapidly accumulate new credit after bankruptcy.

But why?

It’s because if you take on too much too quickly, then it can put a huge financial strain on you. There is a high chance it’ll jeopardize the recovery process.

Payday Loans

Be cautious when using high-cost credit options. Some people think that options like payday loans are particularly beneficial.

But is that true?

Not 100%. They offer quick cash, but interest rates can lead to a never-ending cycle of debt. So it’s best to stay away from it.

Not monitoring your credit

Check your credit report regularly. It maintains the accuracy of your credit information and ensures a smoother recovery process.

If you don’t you may find that it takes longer to rebuild from bankruptcy, or worse, find yourself needing to file for bankruptcy again!

Strategies for Accelerated Credit Rebuilding:

Understand how various types of credit impact your credit score. For example, having a credit mix, such as credit cards, installment loans (like car loans), and mortgages, can positively impact your credit score. Your credit utilization ratio, or the percentage of available credit you use, is crucial.

Keeping credit card balances low relative to your credit limit can positively impact your score. Here are some tips on using credit wisely to avoid high-interest debt.

- Consider seeking financial advice for informed credit decisions.

- Be aware of and stay well below credit limits to avoid high utilization.

- Thoroughly review terms and conditions to understand fees and penalties.

- Pay credit card balances in full each month to prevent interest accumulation.

- Build and maintain an emergency savings or fund to cover unexpected expenses.

Another way to rebuild credit is by using financial products. You can use secured credit cards, share-secured loans, retail credit cards, debt consolidation loans, prepaid credit cards, etc. However, ensure you use these responsibly, make timely payments, and choose options aligned with your financial goals.

Long-Term Credit Health Maintenance

You should maintain a low credit utilization ratio to achieve long-term credit health. What is it?

It’s the percentage of credit used compared to the total available.

Lower ratio = Positive impact on credit scores.

But there’s another factor that has a massive impact on creditworthiness.

It is the debt-to-income ratio.

It’s the proportion of monthly income devoted to debt repayment. Many lenders use this ratio to assess an individual’s ability to manage additional debt responsibly.

Lower ratio = Better financial stability + Enhances creditworthiness.

However, even after being bankrupt 100 times, an individual will fall into this trap again. Do you know why?

Because they lack financial education and awareness, they cannot maintain credit health in the long run. That’s why we focus on learning more about it.

Conclusion

The first step in rebuilding credit after bankruptcy is often the most transformative. Remember that change is not only possible but achievable. That’s how every positive financial decision you make leads you toward a brighter future.

Increase your credit reputation by applying these strategies for rebuilding your credit.

But every person has a unique journey.

That’s why you need something more than templates and built-in guides. Consult an experienced financial advisor to get a personalized solution to your problems. For more details, visit Credit Secrets and say hello to your financial well-being.

Jenn Cartwright

Jenn is the lead credit coach and head of customer success at Credit Secrets.

She transformed her own credit story from a modest beginning into an inspiring tale of financial triumph using the Credit Secrets program.

Originally a customer back in April 2017, she not only soared her scores from the low 400s to the 700s within 6 months using the Credit Secrets program, but also delved deep into the credit cosmos, exploring courses, consumer laws, and even co-hosting webinars with the nation's leading credit expert, John Ulzheimer.

Now, she funnels her passion and expertise into ensuring everyone has access to clear, concise, and actionable information to improve their credit scores and unlocking their financial freedom.

What's Trending