This is How to Get the Most From Experian Boost Rent +More

Experian Boost offers a way for you to improve your credit scores for free. A little over a year ago, they started offering the option to report rent payments to credit bureaus. Fantastic, right?!

Well, this system poses some relevant questions:

- Can you boost credit by paying rent?

- How much does rent increase your credit score?

- Do landlords even use Experian?

Moreover, some people have a hard time connecting their payments to the system or can’t find their bank in the system. So, let’s take a deep dive into the Experian Boost system and find out how you can maximize this free offer.

Here’s what’s in store:

- What is Experian Boost?

- How to Proactively Optimize Your Experience with Experian Boost

- The Difference Between Experian Boost & Credit Karma

- Frequently Asked Questions

- Conclusion: Is it Worth it to Report Rent to Credit?

Now, let’s go!

What is Experian Boost?

Experian Boost is a free web and mobile app from Experian, one of the three leading consumer credit reporting agencies – the app offers an instant credit score boost to anyone.

The app lets you pump up your credit score by including certain bills that usually don’t get the credit score limelight. Think utility and telecom bills – stuff like electricity, water, gas, cable, internet, phone. Add these payments to your Experian credit report, and bam, you’ve got a shot at giving your credit score a boost.

Now, Experian boost even lets you add rent, insurance, and streaming services like Netflix to your credit report. It’s like giving your credit history a little extra love by recognizing those everyday payments that usually fly under the credit radar. Cool, right?

There is one major catch – Experian Boost will only change your Experian credit score, and will not increase Transunion or Equifax scores.

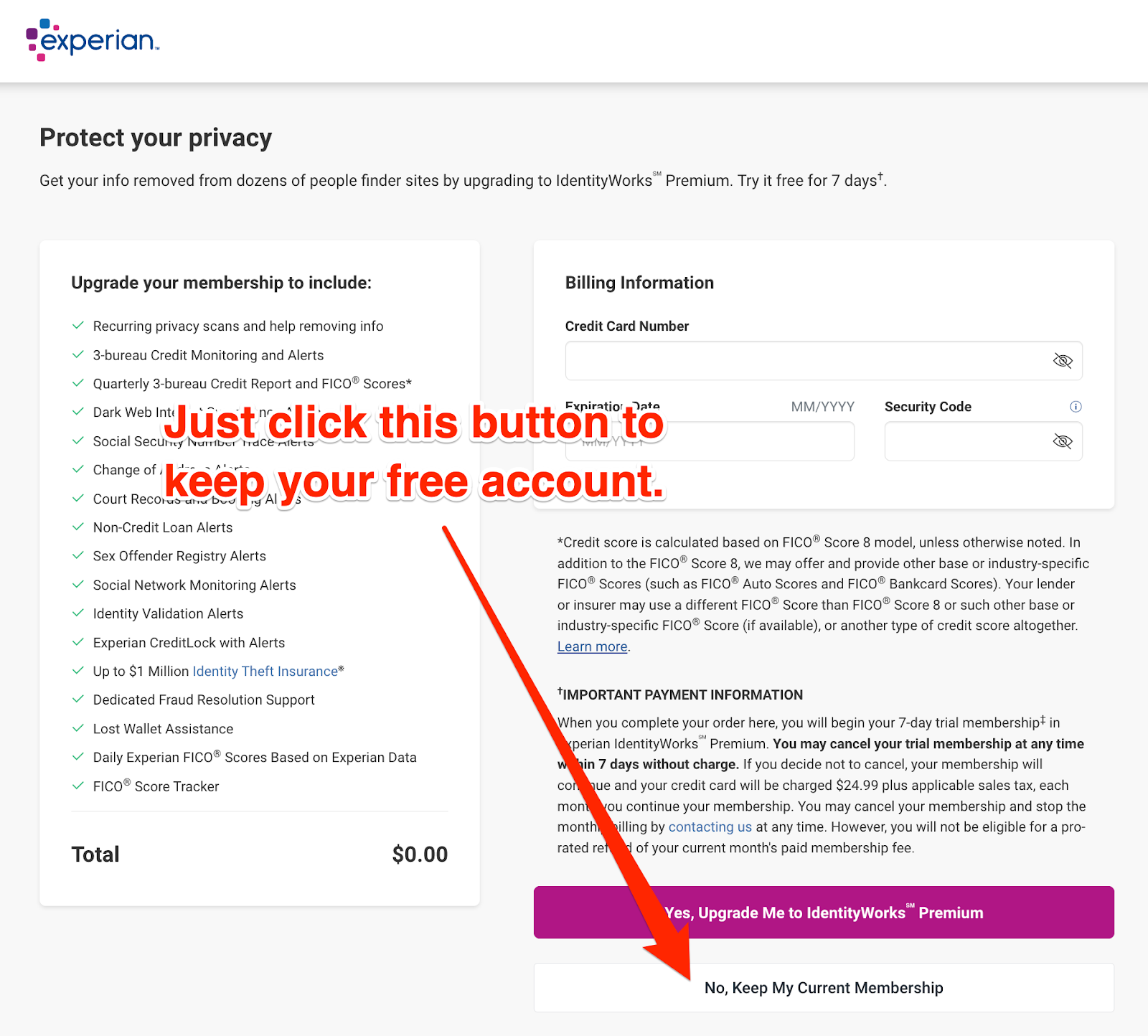

Note that every single time you sign in, you’ll be asked to upgrade your account and offered a 7-day free trial of the premium account features…

…and, unless you want to upgrade, just click the teeny tiny, incognito button at the very bottom of the page that says, “No. Keep My Current Membership.”

You might also like: How Does Self Credit Builder Work? The Big Picture

Experian Boost Rent Payments Overview

Experian Boost now lets you elevate your credit score by adding timely rent payments alongside bills for phone, utility, and streaming services.

It’s a free tool that integrates seamlessly with your bank accounts or credit cards used for bill payments.

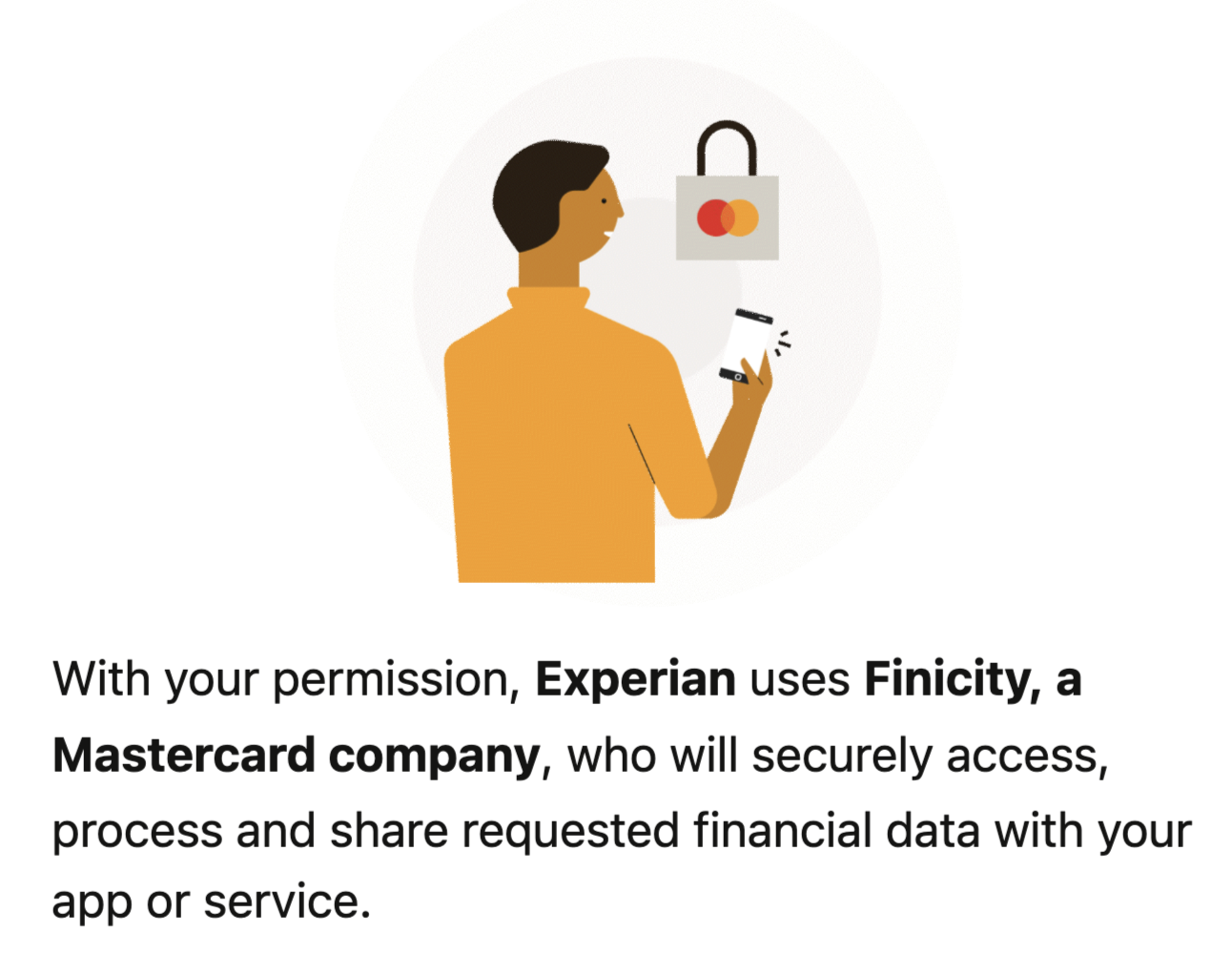

First, you connect your bank account to the platform.

Experian partners with Fincinity to connect to and scan your transactions.

Then, the system:

- Scans your payment history

- Identifies eligible payments

- Gives you the chance to confirm

- Instantly boosts your Experian credit score

To include rent, ensure your payments exceed the qualifying number of payments (at least 3 residential rent payments within 6 months, at least one of those in the past three months), made online to eligible landlords or through a rent payment platform – Unfortunately Venmo payments or checks to your roommate won’t qualify.

In essence, Experian Boost Rent can turn your regular rent payments into a credit-building tool, providing an accessible way to improve your credit score…as long as you meet the requirements.

Recommended: DIY Credit Repair Demystified (It’s Not as Hard as You Think)

How to Proactively Optimize Your Experience with Experian Boost

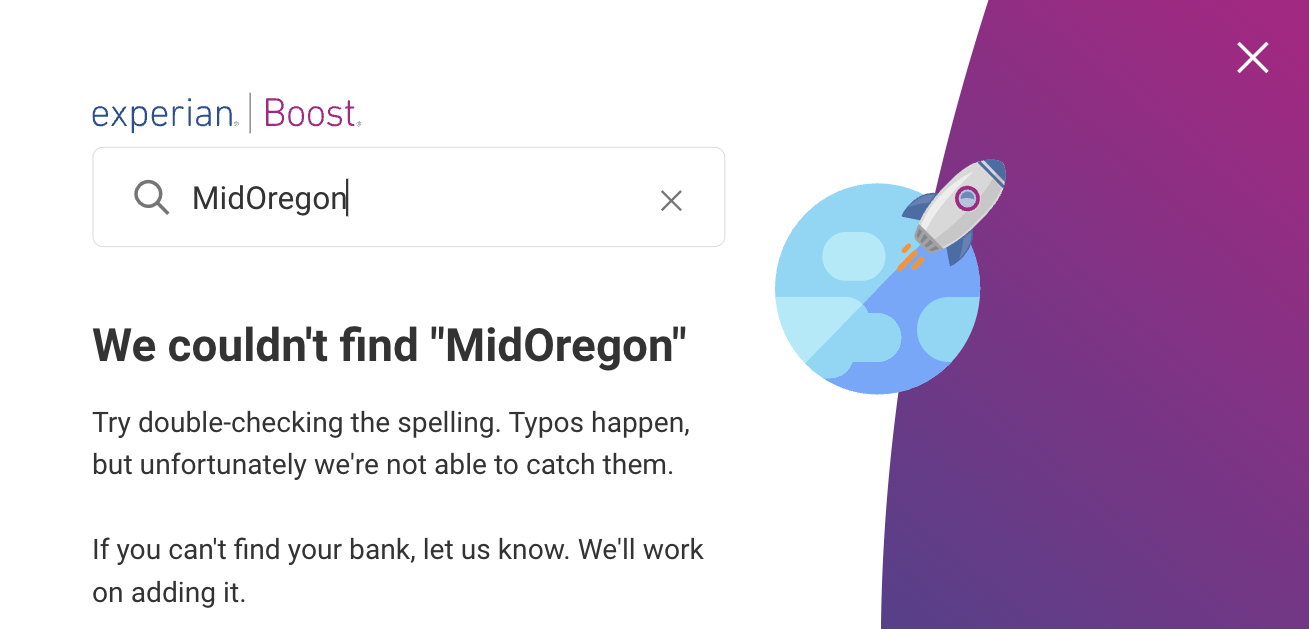

So many people turn and walk when Experian boost wont connect to their bank (i.e. doesn’t cater to their current lifestyle). When they don’t see their bank or credit union on the Experian app, so they bounce.

This makes sense because you know that if you request your small community bank, it’s going to be months (or years) before they add it anyway, right?

Well, no… not right – the truth is, you’re the master of your life, and you can use this tool to level up your credit score if you want to. Take the reins with these tips!

You might also like: How To Build Credit History (The Fastest Way)

1. Choose Rental Partnerships Wisely

When you’re out hunting for homes to rent, prioritize working with companies and individuals who are either already participating in Experian Boost compatible services. And, if that’s not an option, talk to your landlord about accepting payments through a rent payment platform.

A lot of people tend to avoid their landlord like the plague, but it shouldn’t be like this – as with all relationships, there should be open lines of communication with the person or company you rent from. rapport is key.

Not only will choosing credit-savvy and personable rental partnerships increase your chances to get rent reported, but also give you the peace of living in a home managed by someone with whom you have mutual understanding.

2. Pay Your Landlord Directly

As you already know, those CashApp payments you made to Blake and Sarah for the past few months aren’t going to help you improve your credit score with Experian Boost. So, get on the lease and make your payments directly to the landlord or property management platform – no more intermediaries.

If you do this, you can make it possible for the Experian platform to see your rent payments and build a connection with your landlord.

3. Use a Second Account for Rent and Bills

Maybe Experian Boost doesn’t have your current bank in their system, or maybe you just don’t want anyone to have their eyes on your personal spending. If either is the case, consider a second, Boost-compatible checking account for all of your recurring payments.

This can add a couple extra steps to your financial routine, but the payoffs are that you can:

- Get your payments reported to Experian Boost

- Protect your personal spending privacy

- Take more control over your finances

If you’re not already on-board this train, look into high-interest checking accounts that can wield even more financial growth.

The Difference Between Experian Boost & Credit Karma

Some people want to know the difference between Experian Boost and Credit Karma. The truth is that these systems are quite different and can be used together.

Experian Boost, a service from the Experian credit bureau, directly impacts your Experian credit report by incorporating alternative data like utility and telecom payments. It aims to boost your Experian credit score.

On the other hand, Credit Karma, now part of Intuit, is a third-party credit monitoring service that provides insights and scores from TransUnion and Equifax. While Credit Karma offers credit monitoring features, it doesn’t directly influence credit reports or scores.

Experian Boost focuses on enhancing your Experian credit profile, while Credit Karma provides a broader view of your credit health across multiple bureaus.

You might also like: Unusual Reasons Your Credit Scores Are Not Higher

Frequently Asked Questions

Do landlords check Experian or Equifax?

Yes, landlords (though not all of them) do check Experian, Equifax, and Transunion when running credit reports for potential renters. Your credit score can impact your ability to rent a home, and your rental history will carry the most weight with homeowners and property managers who consider renting to you.

What bills qualify for Experian Boost?

Experian Boost considers utility and telecom bills for boosting your credit score. These bills can include services like electricity, water, gas, cable, internet, phone, and even streaming services. Adding these payments to your Experian credit report has the potential to positively impact your credit score.

What is Experian RentBureau?

Experian RentBureau is a division of Experian, one of the major credit reporting bureaus. Specializing in collecting and reporting rental payment information, RentBureau allows landlords and property management companies to report tenant rental payment data. This data, when included in credit reports, can contribute to improving your credit score.

Why can’t I add my rent to Experian Boost?

Several factors can throw a wrench in your ability to add rent to Experian Boost. Troubleshoot by checking for Incorrect or insufficient information. Look for a non-participating bank or credit union. Make sure your payments were made to an eligible landlord or rent platform. And, look at technical issues including your browser’s privacy settings. If you can’t fix it yourself, reach out to Experian for help.

Does Experian Boost help with mortgage?

Mortgages are typically reported to credit bureaus each payment period, so there is no need to use a service like Experian Boost for monthly house payments.

Conclusion: Is it Worth it to Report Rent to Credit?

Morally (and probably legally), I can’t advise whether it would be worthwhile for you to report your on-time rent payments to the credit bureaus. As a homeowner, my mortgage is reported, and my positive payment history on a combination of loans and credit cards is enough that I haven’t needed a service like Experian Boost.

What I can say is that, when my credit score was low (at one point, it was 350!), if a service like this would have been available, I probably would have used it. However, I still would have had to clean up the riff raff on my credit report — these types of services do not help you repair negative items on your credit report.

Experian Boost is free, and the only risk with a free account is that you give the corporation and their partners access to your bank account – if you’re comfortable with that as it stands (or if you want to take the advice above and be more deliberate with your banking practices), you might be good-to-go.

To get that credit score up fast so you can move forward with your life, check out Credit Secrets and start your journey to better financial health.

Ashley Kimler

Ashley Kimler is your friendly Credit Secrets wordsmith. With a knack for turning complex money matters into easy-to-digest advice, Ashley has been a trusted voice in the world of finance. With writing credits from Pangea Money Transfer, Centier Bank, Performio, and more, she's here to help you navigate the financial jungle with a dollop of wisdom. Let's turn sense into dollars together!