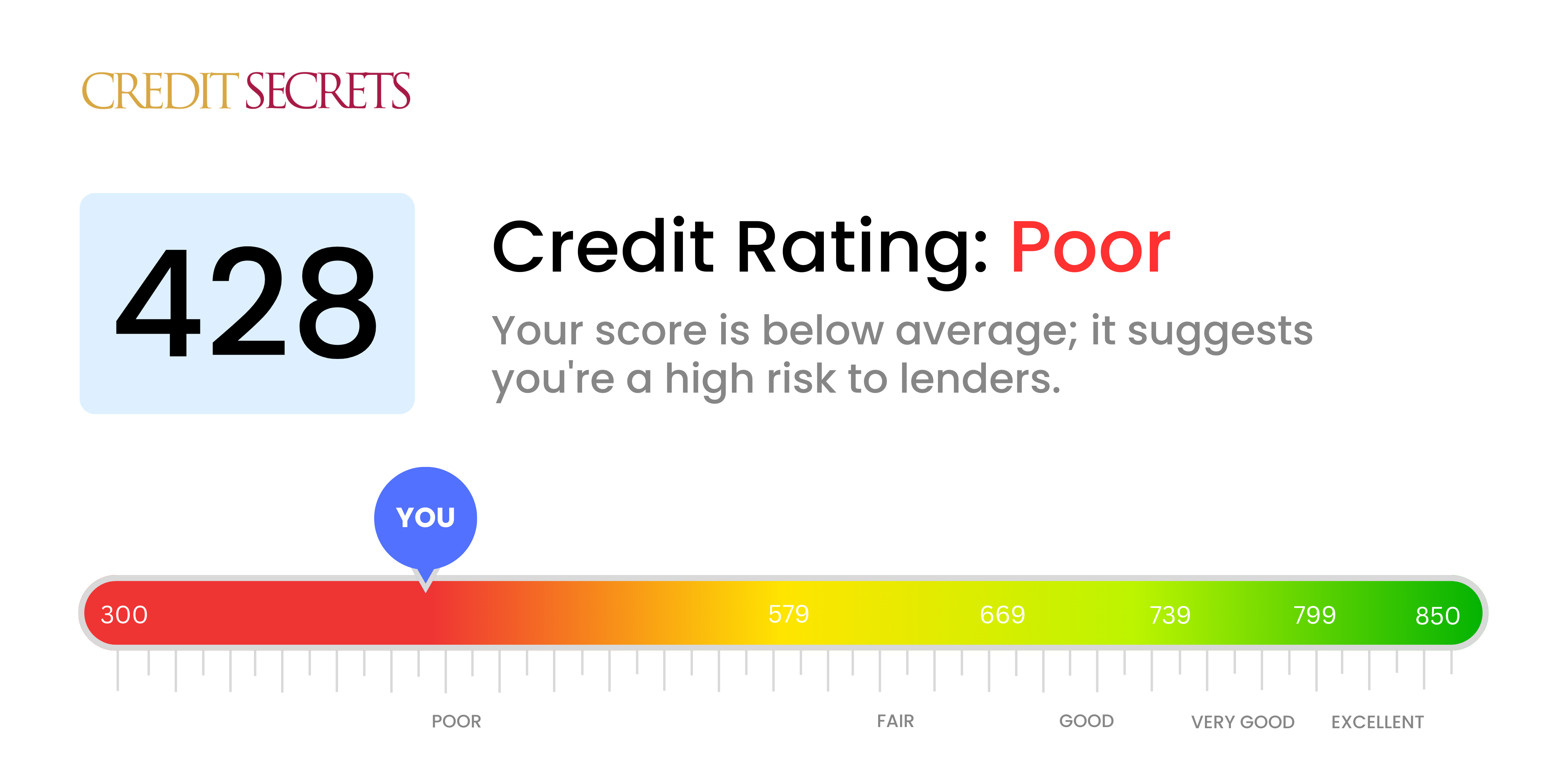

Is 428 a good credit score?

Unfortunately, a credit score of 428 isn't optimal as it falls within the 'poor' category in the credit score spectrum. This could limit financial opportunities, making things like getting approved for loans or credit cards more challenging, and interest rates on these could be high due to the perceived risk. However, know that it's entirely possible to raise your score with focused efforts and strategic financial decisions.

Improve your financial outlook by utilizing resources and tools to boost your credit health and establish better credit practices. Repairing your credit isn't an overnight process, but by making consistently on-time payments, reducing debt, and making smart financial decisions, you can start to see improvements. Remember, everyone's financial journey is unique, but a lower credit score doesn't define your financial future.

Can I Get a Mortgage with a 428 Credit Score?

If you find yourself with a credit score of 428, you might encounter difficulty gaining approval for a mortgage. Lenders usually search for scores well above this mark, and as such, a score of 428 can suggest previous financial trouble like late payments or defaults.

Being in this situation can feel disheartening, but it's important to know that there are potential alternatives to consider. You might contemplate applying for a Federal Housing Administration (FHA) loan which stipulates lower minimum scores for qualification. Additionally, having a solid history of on-time bill payments, a stable income, as well as a significant down payment, can bolster your chances of being approved. Despite the difficulty, homebuyers with lower credit scores have been able to secure mortgages. Progress may be slow, but your financial future can still be bright!

Keep in mind that a lower credit score like 428 might lead to higher interest rates. This is another reason why focusing efforts on improving your credit over time is paramount. Remember, circumstances can change and with persistence, so can your credit score.

Can I Get a Credit Card with a 428 Credit Score?

With a credit score of 428, getting approved for a conventional credit card can be a significant hurdle. Banks and lenders often see this score as a sign of previous financial struggles or mismanagement. It's a tough pill to swallow, but acknowledging the reality of your credit situation is a crucial step towards improving your financial health.

Don't lose hope, there are other possibilities you might want to consider. A secured credit card, for example, is an option that can be easier to qualify for given your credit score. These cards entail a deposit that acts as your borrowing limit and can provide a pathway to rebuilding your credit. Alternatively, a co-signer or a pre-paid debit card could also be suitable for your needs. Bear in mind though that these options are not quick fixes, but tools that can help you over time in your journey to better fiscal stability. Note that any credit you can secure with a score like yours is likely to have a higher interest rate due to the perceived risk by lenders.

Unfortunately, a credit score of 428 falls significantly below what most traditional lenders require for approval of a personal loan. It's a tough situation, but it's critical to acknowledge that this score portrays a high risk to lenders. Therefore, it is improbable that you would secure a loan in standard terms. This, though challenging, simply means your borrowing options might need to be a bit different.

If conventional loans are out of reach, you might explore other possibilities like secured loans where you provide an asset as collateral, or co-signed loans, where someone else with a stronger credit score supports your application. Another avenue could be peer-to-peer lending platforms that can sometimes offer more lenient credit requirements. Yet, bear in mind these alternatives often have higher interest rates and less favorable conditions due to the amplified risk to the lender. It's a tough road, but remember there are still options and it's always possible to improve your financial situation.

Can I Get a Car Loan with a 428 Credit Score?

Having a 428 credit score can pose a tough situation when trying to secure a car loan. Financial institutions often seek credit scores above 660 to offer favorable lending terms, with scores falling below 600 typically viewed as high-risk. With a 428 score, you're in this higher risk category which could lead to rejection or excessive interest rates. This is because your credit score reflects a perceived risk to lenders - a low score indicates a history of difficulties in repaying borrowed funds.

Yet, remember this doesn't necessarily mean the end of the road for your car ownership ambitions. There are lenders who specialize in granting loans to individuals with lower credit ratings. Just be aware that these partnerships may come with significantly higher interest rates due to lenders wanting to protect their investment. Despite this, with thoughtful assessment and an understanding of loan terms, acquiring a car loan isn't absolutely impossible. Stay hopeful and remember that credit scores can always be improved over time.

What Factors Most Impact a 428 Credit Score?

Grasping the reasons behind a score of 428 can seem daunting, but it's the first step towards building a better financial future. By recognizing and focusing on the factors that are likely influencing your score, you can start charting your path to improved credit.

Credit Payment History

Your credit payment history can greatly affect your score. Late or missed payments are likely significant factors for a score of 428.

How to Check: Look at your credit report. Pay attention to any payments you've made late or missed completely as these can heavily impact your score.

Credit Card Utilization

Your credit card balances might be close to or exceeding their limits, this high credit utilization could be a contributing factor to your low score.

How to Check: Review your credit card statements. Look for high balances relative to your credit limits.

Credit History Length

A shorter credit history might be contributing to your score. Many who have scores in the 400s are either new to credit or haven't been actively using it for long.

How to Check: Examine your credit report for the age of your oldest account and the average age of all your accounts.

Public Records

Public records like bankruptcies and collections can greatly affect your score.

How to Check: Review your credit report for any public records, such as bankruptcies or collections. Resolve any discrepancies you find.

Remember, take each opportunity for growth and learning, and always keep an optimistic outlook.

How Do I Improve my 428 Credit Score?

With a credit score of 428, it’s clear that you’ve encountered financial struggles. But remember, it’s just a number. It doesn’t determine your financial future. Let’s work on this together:

1. Confront Unsettled Debts

Unpaid balances and overdue accounts loom large on your credit score. It’s crucial to settle these as promptly as possible. Start with your most delinquent accounts for maximum effect. Make arrangements with your creditors for payment plans if possible.

2. Manage Your Credit Card Usage

Your credit utilization can make a big difference to your credit score. Try to keep your card balances below 30% of their limit, aiming for 10% in the long term. Remember, it’s the ratio of credit used to credit limit that impacts your score – focus on cards with the highest utilization first.

3. Consider a Secured Credit Card

Given a 428 score, it might be difficult to obtain a traditional credit card. A secured credit card, backed by a cash deposit, can be a useful tool. Treat it like a regular card, maintaining lower balances and paying in full monthly to build positive credit history.

4. Explore Authorized User Status

See if a responsible friend or family member would add you as an authorized user on their credit card. While you aren’t responsible for payments, their good credit behavior can aid your credit score recovery. Always confirm if the credit card company reports authorized user activity to credit bureaus.

5. Expand Your Credit Portfolio

Once you’re managing a secured card responsibly, consider diversifying your credit. A mix of credit types – like credit builder loans or retail credit cards – could help boost your score. Show you can handle different types of credit responsibly.

These steps are the beginnings of your journey to improved credit health. And remember, the path to better credit is not a sprint, but a marathon. Keep going!